Methyl Ethyl Ketone: european price increases under review

Falling chinese prices call into question the sustainability of european price Increases

Published by Daniel Vito Lobasso. .

Organic Chemicals Petrolchimica Price DriversAs already observed in the case of ethanolamines, the European methyl ethyl ketone market — also known as MEK, 2-butanone or butanone — is experiencing a period of strong requests for price increases, often justified by geopolitical risks in the Persian Gulf and the possible consequences of a blockade of the Strait of Hormuz.

Data collected by the Milan Chamber of Commerce show that prices have more than doubled over the past three months. For MEK as well, it is therefore necessary to assess how much of this increase is supported by cost, demand and supply fundamentals, and how much instead reflects expectations, advance purchases and greater bargaining power on the part of sellers.

Limiting the analysis to observable factors, this study will focus on three aspects:

- the evolution of raw material costs and of the petrochemical value chain upstream of MEK;

- the structure of demand and the degree of substitutability of MEK in its main industrial applications;

- the structure of global supply, with particular attention to the role of China, the European market and the possible transmission channels of the crisis in the Persian Gulf.

The production process and costs of methyl ethyl ketone

The first issue to examine concerns the actual impact of the geopolitical crisis on production costs. Methyl ethyl ketone is an oxygenated solvent belonging to the ketone family. From an industrial perspective, its production is linked to the C4 value chain, particularly butene, also known as butylene, and butanols, specifically 2-butanol, also known as sec-butanol or sec-butyl alcohol, from which MEK can be obtained through dehydrogenation processes.

These relationships make it useful to compare the price of MEK with the main benchmarks of its upstream value chain. If the price increase were explained exclusively by higher production costs, a relatively consistent trend would be expected between the price of the finished product and that of the production inputs.

For this purpose, the first principal component of petrochemical platform prices, introduced in the article "An economic classification of the chemical industry", can be used. This indicator can be considered representative of the trend in the average costs of the different MEK production processes.

The following chart shows the intra-EU customs price of MEK and the PC1 factor of the petrochemical value chain, expressed in euros per tonne.

Price of MEK and the PC1 factor of the petrochemical value chain

The comparison confirms that the petrochemical industry experienced an upward phase in the second quarter of 2026, although with significantly lower intensity than MEK. The petrochemical factor therefore indicates a higher-cost environment, but one that cannot, on its own, explain a doubling of methyl ethyl ketone prices.

Uses of methyl ethyl ketone and its degree of substitutability

Demand for methyl ethyl ketone mainly comes from the paints, coatings, inks, adhesives, packaging and technical cleaning sectors. In these applications, MEK is valued for its good solvent power, high volatility and compatibility with numerous resins and industrial formulations.

Overall, the degree of substitutability of MEK can vary considerably depending on the final application: in some formulations, substitution is technically straightforward, while in others, particularly in more specialised applications, the possibilities for substitution are more limited.

In coatings, inks and adhesives, the scope for substitution can be relatively broad, but it is rarely immediate. Acetone, methyl isobutyl ketone, ethyl acetate, butyl acetate and formulated solvent blends may represent alternatives or components of substitute formulations, but the choice depends on resin compatibility, evaporation rate, application performance and the requirements of the final customer.

In technical cleaning and degreasing applications, substitutability is more variable. In some cases, acetone, alcohols or formulated solvents can partially replace MEK, while aromatic, chlorinated and saturated hydrocarbon solvents are more specific alternatives, often limited by technical, regulatory or safety constraints.

In formulations requiring a more controlled solvent power, cyclohexanone and certain glycol ethers may represent partial substitutes, but with different evaporation and usage profiles. Consequently, substitution is possible, but it cannot be interpreted as an automatic and immediate switch from one solvent to another.

The following chart shows the prices, in euros per tonne, of MEK and the main solvents that can fully or partially replace it in industrial formulations:

- methyl ethyl ketone;

- acetone;

- methyl isobutyl ketone (MIBK);

- ethyl acetate;

- n-butyl acetate;

- cyclohexanone.

Price of MEK and its main substitutes

Between March and June 2026, acetone and cyclohexanone recorded increases of around 20%, confirming a certain degree of tension in the solvent market. However, ethyl acetate and methyl isobutyl ketone did not show movements comparable to those of MEK. Butyl acetate also increased, but much less sharply than methyl ethyl ketone.

The comparison with MEK substitutes reveals a complex picture, in which substitute prices tend to follow heterogeneous trends. If the increase had been driven by generalised pressure on alternative solvents, a more synchronised movement between MEK and its substitutes would have been expected.

However, although substitution is not immediate in the short term, over the medium term the availability of technically viable alternatives has the potential to limit increases in MEK prices.

Global supply and the European methyl ethyl ketone market

The third area of analysis concerns the structure of global supply, the European market and the transmission channel represented by China.

The following charts show the main MEK supplier countries globally and for the EU (source: ExportPlanning).

Main MEK supplier countries by destination market

| World | EU |

|

|

China is the world's leading exporter, with approximately 200 thousand tonnes exported in 2025, equivalent to around one-third of global trade. EU countries also retain a significant role as an exporting region, accounting for close to one-quarter of global trade. Overall, China and Europe therefore represent more than half of international MEK trade.

As regards the composition of European supplies, in 2025 more than 95% of European MEK imports were supplied by just seven countries. In particular, the United Kingdom alone accounted for slightly more than 30% of volumes, followed by the Netherlands and Belgium, which also play an important role as commercial and logistics hubs. China accounted for slightly more than 8%, followed by South Africa and Japan.

The Chinese channel, however, deserves particular attention. In addition to being the world's largest MEK exporter, China is also one of the leading global producers, and its petrochemical system is heavily dependent on flows of energy raw materials from the Persian Gulf. In 2025, more than 60% of China's imports of liquefied butanes came from the United Arab Emirates, Saudi Arabia, Qatar and Kuwait.

The following chart compares the price of liquefied butanes imported by China with Chinese MEK prices recorded by two different sources: the FOB price of Chinese exports and Over-The-Counter (OTC) market quotations collected by SunSirs.

Price of Chinese MEK and its input

As shown in the chart, the period of heightened geopolitical tension coincided with a sharp increase in both Chinese import prices for liquefied butanes and MEK prices.

The magnitude of the increases, however, varied significantly. Between February and May 2026, the FOB price of MEK rose by 33%, compared with a 60% increase in liquefied butane prices. Over the same period, SunSirs OTC assessments recorded an even stronger increase of more than 75%, reaching a four-year high in April. The divergence between OTC assessments and MEK FOB prices indicates that the rally was likely driven not only by higher feedstock costs, but also by additional supply-side constraints and temporary market tightness. OTC prices subsequently reversed course and continued to decline in June, settling at slightly above EUR 1,000 per metric tonne. This correction occurred despite the ongoing conflict in the Persian Gulf, which continued to provide support to liquefied butane prices. The price movement therefore suggests that the temporary factors that had amplified the earlier OTC rally gradually eased, allowing market fundamentals to rebalance.

To assess the likely trend of European MEK prices over the coming months, it may be useful to compare international prices recorded by four different sources:

- intra-EU customs prices;

- prices from the Milan Chamber of Commerce;

- FOB customs prices of Chinese exports;

- Chinese Over-The-Counter (OTC) market prices recorded by SunSirs.

Price of European and Chinese MEK

The comparison shows that international MEK prices are characterised by very similar trends, with Chinese prices tending to anticipate price developments in European markets. In the current phase as well, Chinese prices appear to be anticipating a decline, acting as a moderating force on international prices and limiting the sustainability of current European price levels.

Conclusions

The analysis of the fundamentals confirms that the increase in MEK prices is supported by higher costs. However, this factor alone does not appear sufficient to justify a doubling of European prices. The most significant signal comes from China, where OTC prices, after anticipating the market tensions, have fallen sharply, while European quotations have remained high.

The most likely scenario is therefore for European prices to remain elevated in the short term, but with a growing likelihood of a correction over the coming months.

Would you like to stay up to date on commodity market trends?

Subscribe to the PricePedia newsletter free of charge!

You may be interested in:

Effects of the reopening of the Strait of Hormuz on prices in the petrochemical supply chains

Published by Luca Sazzini. .

Petrolchimica ForecastFrom an energy shock to normalization? What PricePedia’s structural models indicate [ Read all ]

An Economic Classification of the Chemical Industry

Published by Daniel Vito Lobasso. .

Organic Chemicals Specialty chemicals Inorganic Chemicals Petrolchimica Analysis tools and methodologiesLa mappa per l’analisi dei prezzi: dalle relazioni chimiche alle relazioni economiche [ Read all ]

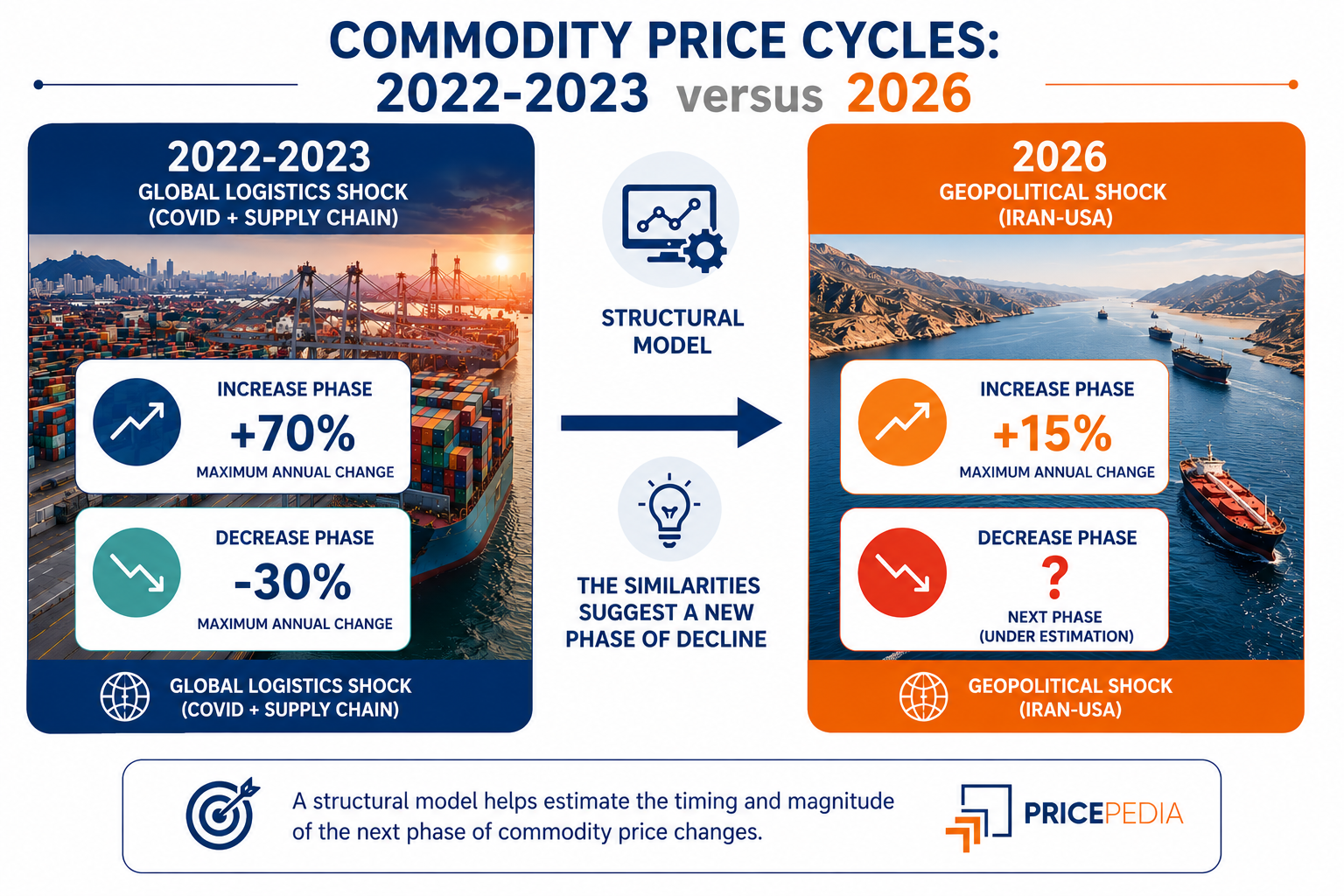

From the 2022-2023 Commodity Cycle to 2026: Insights from Structural Models

Published by Luigi Bidoia. .

Organic Chemicals Petrolchimica Strait of HormuzIl confronto tra i due shock energetici consente di stimare quali commodity potrebbero registrare le maggiori riduzioni di prezzo nei prossimi mesi [ Read all ]