Effects of the reopening of the Strait of Hormuz on prices in the petrochemical supply chains

From an energy shock to normalization? What do PricePedia’s structural models indicate?

Published by Luca Sazzini. .

Petrolchimica Forecast

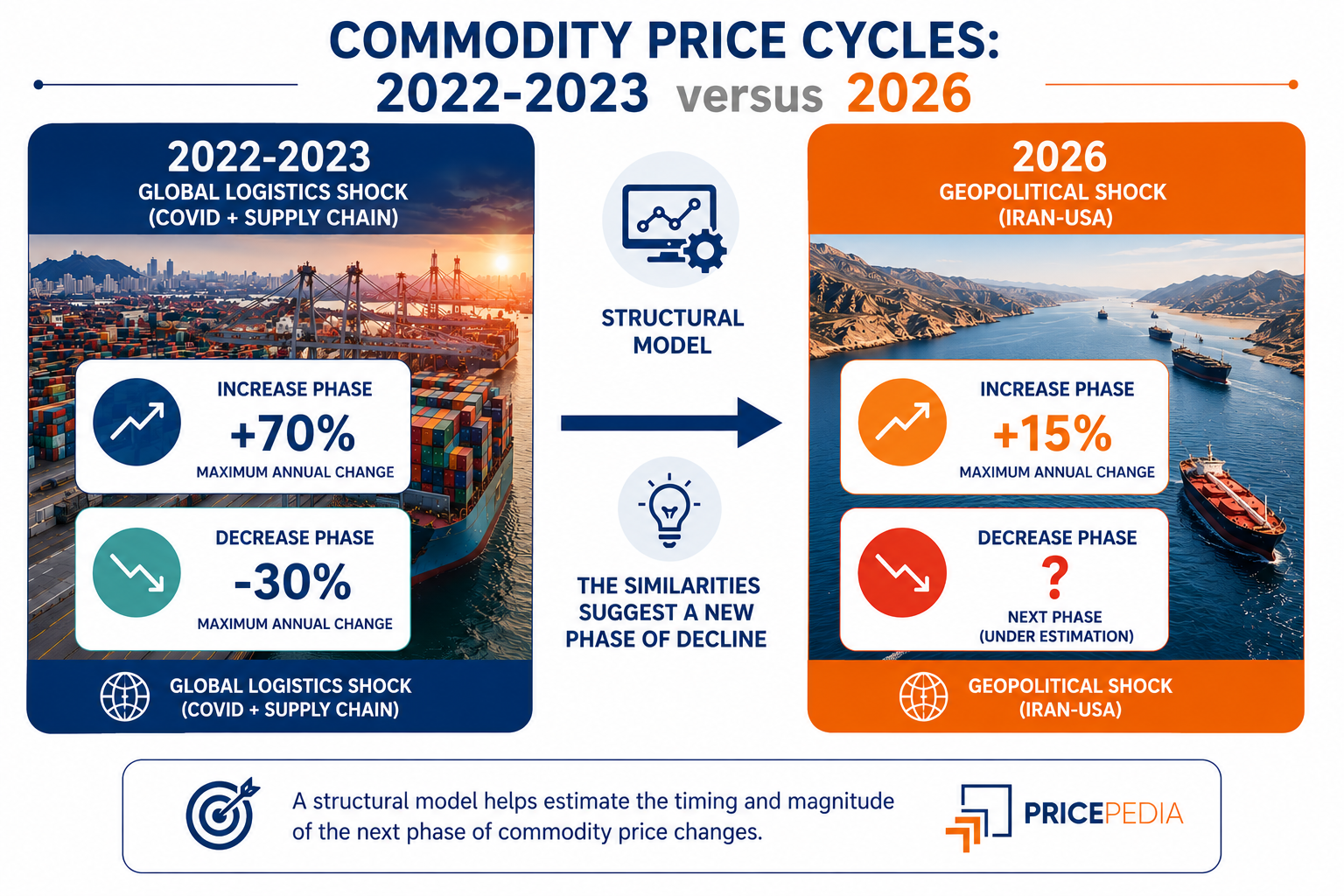

The escalation of the conflict between the United States and Iran and the resulting closure of the Strait of Hormuz pushed Brent oil financial prices up to $118/barrel, levels close to those reached during the 2022 energy shock, when the daily closing price hit a relative peak of $124/barrel.

The increase in international energy prices spread across the various production chains through both direct and indirect transmission mechanisms, exerting significant upward pressure, especially on petrochemical commodity prices. In particular, as highlighted in the analysis: “FFrom the 2022-2023 Commodity Cycle to 2026: Insights from Structural Models”, the prices of thermoplastic polymers, hydrocarbons, and alcohols were among those that were most affected by the increase in energy feedstock costs and, consequently, could be particularly sensitive to the recent decline in energy prices observed in recent days.

The gradual improvement in the geopolitical situation, following the memorandum of understanding between the United States and Iran and the reopening of the Strait of Hormuz, led to a rapid decline in Brent financial prices, which returned to levels close to $70/barrel, similar to those recorded before the conflict.

In this context, it may be useful to analyse the evolution of petrochemical commodity prices in light of the information currently available.

PricePedia Forecast

The following chart shows the PricePedia forecast scenario for the aggregated indices of thermoplastic polymers, hydrocarbons, and alcohols, based on the information available as of 2 July.

PricePedia forecast scenario for the aggregated indices of thermoplastic polymers, hydrocarbons, and alcohols, expressed in euros

The structural models developed by PricePedia outline a price reduction scenario for the three aggregated indices considered, consistent with expectations of a gradual recovery in trade flows through the Strait of Hormuz.

Given expectations of temporary tensions that will support prices in the short term, the thermoplastic polymers index is the one for which the most significant contraction is forecast over the following two years, with a decrease of approximately -14% between June 2026 and June 2028.

Over the same time horizon, hydrocarbons and alcohols are instead expected to experience more moderate declines, of around -8%.

The larger expected reduction in thermoplastic polymer prices reflects the stronger increase recorded following the latest energy shock, which began in March 2026. Between February and June 2026, in fact, thermoplastic polymer prices increased by +44%, with rises almost twice as large as those observed for hydrocarbons and alcohols.

The main risk factors for this forecast scenario concern the evolution of the agreements between the United States and Iran, particularly with regard to the possible introduction of a transit fee for ships passing through the Strait of Hormuz and developments in the Iranian nuclear dossier, as well as the speed of restoration of trade flows through the Strait of Hormuz.

Forecast scenario for petrochemical chain products

The following table reports, for each of the three aggregated indices considered, the price variations of selected representative products, relating them to the dynamics of financial prices of crude oil and natural gas. The analysis considers two distinct time periods: February - June 2026, aimed at highlighting the effects of the energy shock resulting from the conflict between the United States and Iran, and June 2026 - June 2028, corresponding to the forecast scenario developed by PricePedia.

Table of percentage price variations expressed in euros

| February 26 - June 26 | Forecast June 26 - June 28 | ||||

|---|---|---|---|---|---|

| Financial prices of production inputs | |||||

| F-Forecast Scenario-Brent (ICE) | +46.76 | -25.88 | |||

| F-Forecast Scenario-Natural Gas TTF (Netherlands) (ICE) | +50.71 | -45.88 | |||

| EU customs prices of petrochemical chains | |||||

| Thermoplastic polymers | |||||

| D-Forecast Scenario-HDPE Polyethylene | +62.32 | -22.22 | |||

| D-Forecast Scenario-Polypropylene (PP) | +58.78 | -22.77 | |||

| Alcohols | |||||

| D-Forecast Scenario-Methanol | +42.57 | -26.44 | |||

| Hydrocarbons | D-Forecast Scenario-p-Xylene | +37.67 | -22.14 | ||

| D-Forecast Scenario-Benzene | +17.47 | -10.50 | |||

The analysis of the table shows that petrochemical commodity prices, which increased by an average of at least 37% following the February - June 2026 energy shock, are expected to decline by more than -20% over the next two years.

Among the analysed commodities, the most significant increases between February and June 2026 concerned thermoplastic polymers, with HDPE polyethylene and polypropylene recording price increases even higher than those of Brent crude oil and European TTF natural gas. This trend can be attributed not only to the increase in feedstock costs but also to the contraction in thermoplastic supply from the Persian Gulf countries, an area that alone accounts for more than 10% of global thermoplastic production.

By June 2028, the final period of the PricePedia forecast scenario, Brent financial prices are expected to realign with the average levels recorded in February 2026, while TTF prices are expected to decline compared with pre-conflict values. Petrochemical chain prices, although expected to decrease significantly, are forecast to remain above the February 2026 average.

You may be interested in:

An Economic Classification of the Chemical Industry

Published by Daniel Vito Lobasso. .

Organic Chemicals Specialty chemicals Inorganic Chemicals Petrolchimica Analysis tools and methodologiesLa mappa per l’analisi dei prezzi: dalle relazioni chimiche alle relazioni economiche [ Read all ]

From the 2022-2023 Commodity Cycle to 2026: Insights from Structural Models

Published by Luigi Bidoia. .

Organic Chemicals Petrolchimica Strait of HormuzIl confronto tra i due shock energetici consente di stimare quali commodity potrebbero registrare le maggiori riduzioni di prezzo nei prossimi mesi [ Read all ]

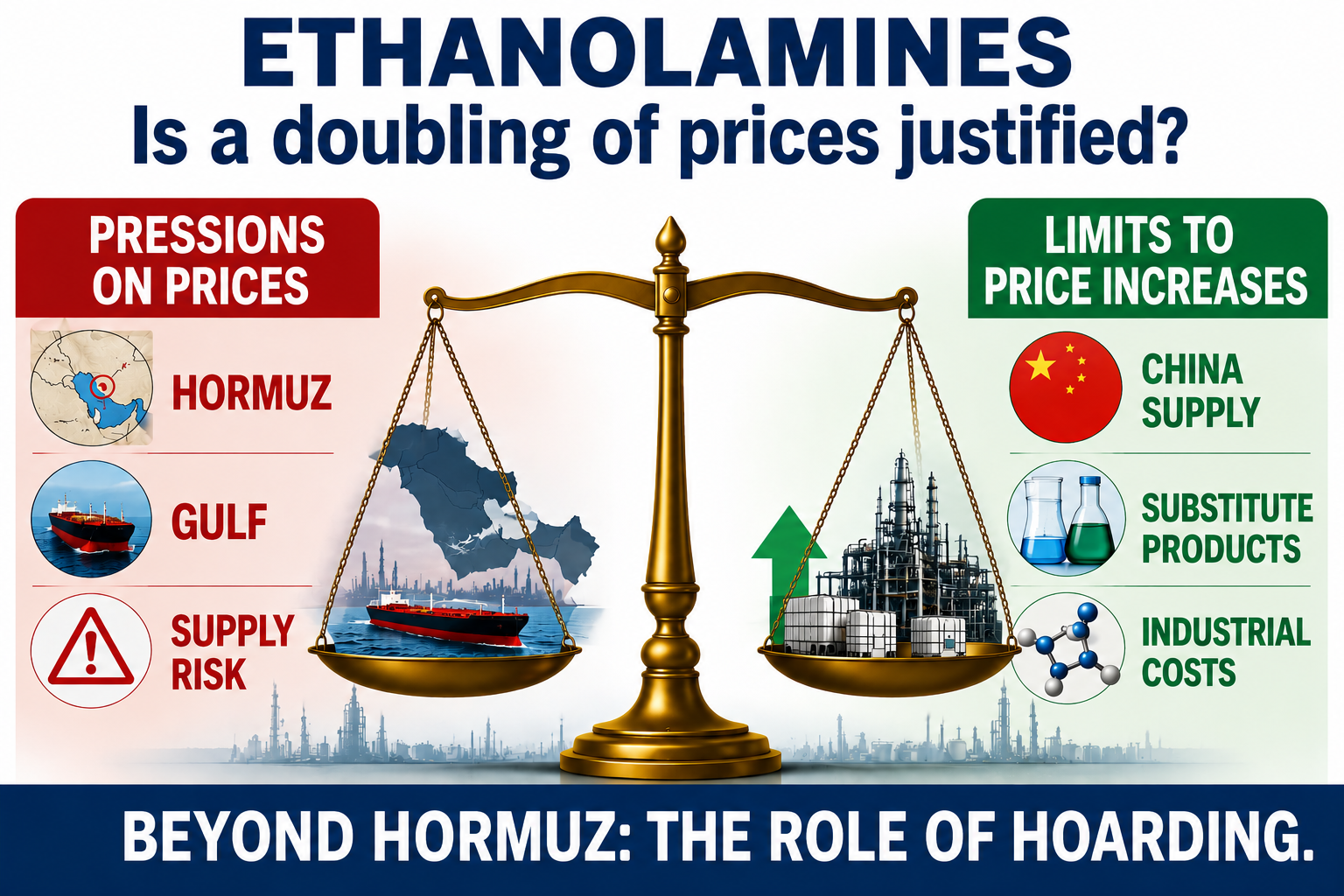

Ethanolamines: Between Market Fundamentals and Supply Concerns

Published by Daniel Vito Lobasso. .

Petrolchimica economic analysis Strait of HormuzGli aumenti di prezzo sono realmente giustificati dal rischio di blocco dello Stretto di Hormuz? [ Read all ]