Sulfuric Acid: Sulfur Sets the Price

The decline in Chinese OTC sulfur prices following the partial reopening of the Strait of Hormuz signals a reduction in the geopolitical premium

Published by Daniel Vito Lobasso. .

Inorganic Chemicals Strait of HormuzDuring May and June, the upward phase in international sulfur prices continued. In particular, both European and Chinese prices reached new historical highs.

The following chart shows sulfur prices from three different sources:

- intra-EU customs prices

- CIF customs prices of Chinese imports

- Chinese Over-The-Counter (OTC) market prices reported by SunSirs.

Comparison of sulfur prices between the European and Chinese markets

In the European market, starting from April 2026, prices recorded overall increases of more than +20%, rising above 460 euros per tonne in June. In the Chinese market, over the same period, increases exceeded +40%, with levels higher than European prices, pointing to stronger tension in the Asian market.

This tension is also clearly visible in the trend of Chinese daily OTC prices, which reached a historical peak on June 15, exceeding 1,400 euros per tonne, before falling and remaining below 1,200 from June 17 until the end of the month.

The decline in the Chinese OTC market represents an initial sign of correction, attributable to a reduction in the geopolitical risk linked to the blockage of the Strait of Hormuz and to an improvement in operators’ expectations regarding an increase in global sulfur supply.

However, the decrease in the Chinese OTC price remains relatively limited and short-lived. It is mainly linked to geopolitical factors, whose easing is still insufficient to bring prices back to the levels seen before the current structural phase of the global industrial cycle.

As reported in the article 800 euros for one tonne of sulfur? This is not a sustainable price, published last May, the global sulfur market is influenced by a plurality of factors. Geopolitical tensions are in fact only a short-term element affecting a market that is already structurally sensitive, where the following factors also play a role:

- demand from the fertilizer and phosphate chemical supply chains;

- availability of supply;

- maritime logistics;

- inventory levels;

- distribution and commercial margins.

Uncertainty in sulfur is being transferred to the sulfuric acid market

Tensions in the sulfur market are also reflected in sulfuric acid, one of the chemical intermediates most widely used by industry.

The following chart shows sulfuric acid prices from three different sources:

- intra-EU customs prices;

- FOB customs prices of Chinese exports;

- wholesale prices reported by the Chemical Products Price Commission of the Milan Chamber of Commerce (CCIAA).

Comparison of sulfuric acid prices between the European and Chinese markets

As shown in the chart, between May and June sulfuric acid prices continued to move upward in both China and Europe, confirming the transmission of upstream pressures along the supply chain.

In particular, Chinese customs prices recorded increases close to +30%, reaching the historical highs of 2022, equal to 129 euros per tonne. This trend reduced the differential compared with the corresponding European prices, which over the same period showed more contained increases, averaging around 6% month-on-month.

The greater tensions in the Chinese market confirm a significant regional component, due to the high logistics costs of sulfuric acid, which limit the full integration of global markets and prevent direct price transmission.

Nevertheless, the signals coming from the Chinese market cannot be ignored for three reasons:

- China is the world’s leading exporter of sulfuric acid, with a share equal to 11.5% of global trade;

- China depends significantly on sulfur from the Persian Gulf, with the United Arab Emirates accounting for 14.1% of its sulfur imports;

- The United Arab Emirates is the world’s leading exporter of sulfur, with a share equal to 24% of global trade.

These characteristics make Chinese prices for sulfuric acid and sulfur fundamental benchmarks for the global market, capable of making changes in global expectations on costs and availability visible in advance. In this sense, the Chinese OTC sulfur price should be read as a leading indicator of upstream pressure, rather than as a value capable of mechanically forecasting the European sulfuric acid price.

As for CCIAA sulfuric acid quotations, which are representative of distribution prices in the European final market, they followed a growth trajectory more similar to the one incorporated by Chinese prices, exceeding 390 euros per tonne in June, with a 10% increase compared with the previous month.

This latest increase further widened the differential between CCIAA prices and intra-EU customs prices, highlighting how the current market situation is characterized by a high degree of uncertainty.

In summary

For buyers of sulfuric acid, monitoring the sulfuric acid market alone is not enough. The tensions that appear in final prices often originate earlier in sulfur, where expectations on costs, availability and supply risk are formed and then transmitted along the supply chain.

News of improving relations between the U.S. and Iran may reduce price increase requests linked exclusively to geopolitical risk. However, it does not yet provide a solid basis for expecting a rapid decline in sulfuric acid prices. The market has corrected part of the short-term premium on sulfur, but it has not yet shown a structural easing of upstream pressures.

The key point to verify over the coming months will therefore be the persistence of the movement. If sulfur prices were to continue correcting and there were an improvement in the physical availability of sulfuric acid, a more favorable scenario for purchases could open up. In the absence of these signals, the June decline in Chinese sulfur prices will remain more a factor of stabilization for sulfuric acid prices within an upward cycle than the beginning of a true trend reversal.

Do you want to stay up-to-date on commodity market trends?

Sign up for PricePedia newsletter: it's free!

You may be interested in:

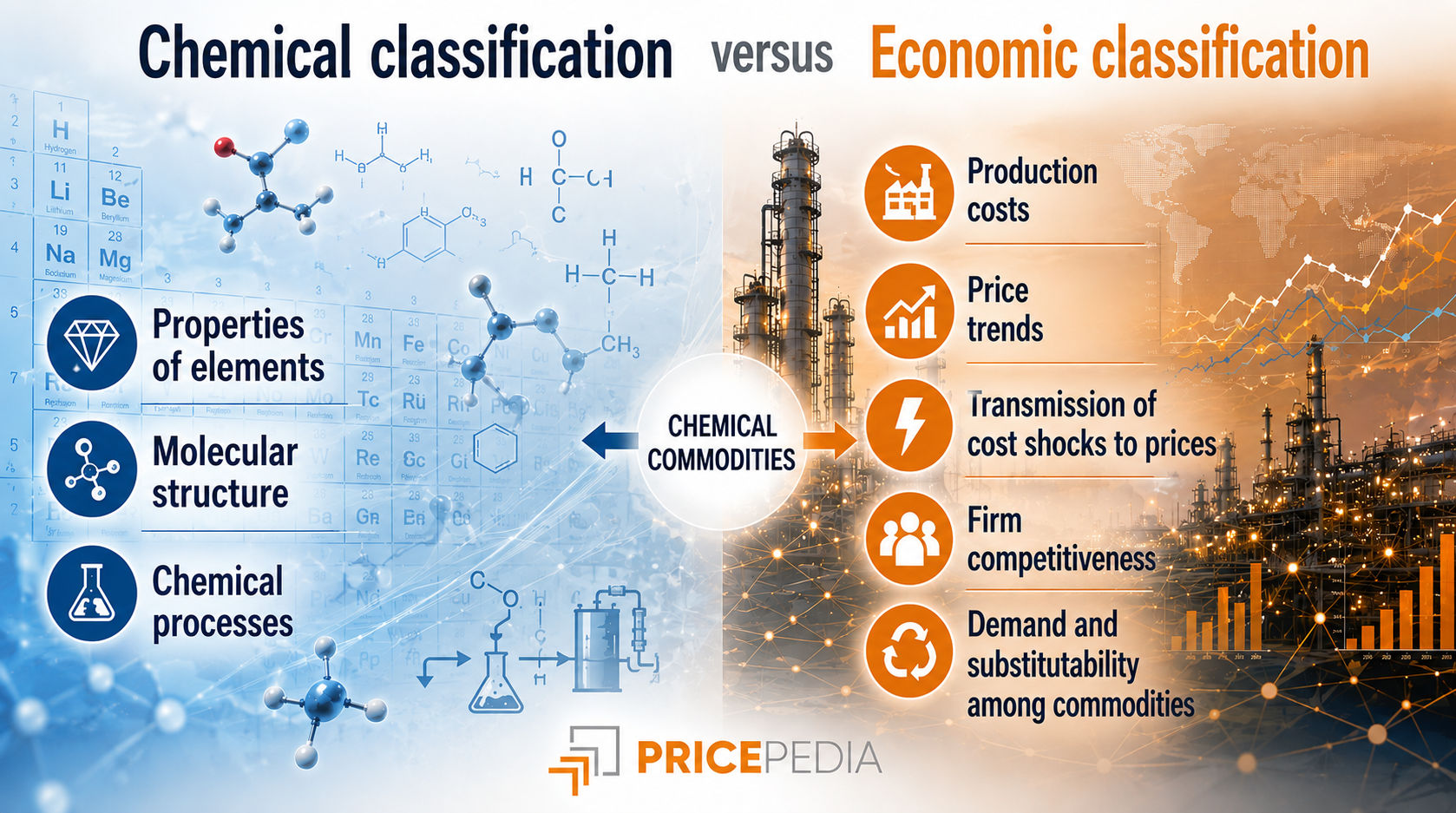

An Economic Classification of the Chemical Industry

Published by Daniel Vito Lobasso. .

Organic Chemicals Specialty chemicals Inorganic Chemicals Petrolchimica Analysis tools and methodologiesLa mappa per l’analisi dei prezzi: dalle relazioni chimiche alle relazioni economiche [ Read all ]

Iodine: concentrated supply and a single global price

Published by Pasquale Marzano. .

Inorganic Chemicals Price DriversThe comparison across different geographical areas highlights a common pricing dynamic [ Read all ]

From Iodine to Its Salts: A Market Dominated by a Single Element

Published by Luigi Bidoia. .

Inorganic Chemicals Cost pass-throughHigh prices and a significant mass contribution make iodine the key cost driver of its salts [ Read all ]