Conflicting signals in regional tungsten prices between Asia and Europe

Analysis of tungsten price trends following Chinese export restrictions

Published by Luca Sazzini. .

Tungsten Critical raw materialsIn the analysis: "How the Chinese market influences the EU market: the case of tungsten and its compounds" the strong concentration of global tungsten supply was highlighted, which depends almost entirely on Chinese output. China, in fact, not only holds the largest global reserves of tungsten ores and alone accounts for more than three quarters of global extraction of the mineral[1], but is also a leader in the production of the main compounds derived from this metal. A disruption or even a simple partial reduction in Chinese exports can therefore be sufficient to generate immediate tensions in global supply, with a consequent increase in international prices and difficulties in procurement along global value chains. This is what has occurred following the introduction by Beijing of new regulatory constraints on the export of certain critical metals, including tungsten.

In February 2025, the Chinese Ministry of Commerce (MOFCOM), in collaboration with the General Administration of Customs, introduced a control system on the export of tungsten and related compounds under the dual-use items regulations, i.e., materials with both civilian and military applications. The new regime requires prior licensing for the export of certain critical raw materials, including tungsten, while simultaneously extending reporting obligations along the supply chain. In particular, access to these materials is made conditional upon the sharing of sensitive industrial data by foreign purchasing companies, including details on production processes, quantities used, and facilities employed for processing derivative products containing critical metals of Chinese origin. This strengthened authorization system allows Chinese authorities not only to regulate exports but also to more systematically monitor the international use of strategic raw materials.

The regime was further tightened in December 2025, when Beijing introduced a system of authorized exporters for the 2026–2027 biennium, limiting to only fifteen Chinese companies the ability to export certain critical metals, including tungsten. In parallel, the licensing system was made more selective and integrated with stricter information requirements, consolidating a model in which not only exports but also the end use of tungsten and other critical raw materials is systematically and structurally monitored.

In light of this progressive tightening of the Chinese regulatory framework, it may therefore be interesting to analyze the evolution of various tungsten prices.

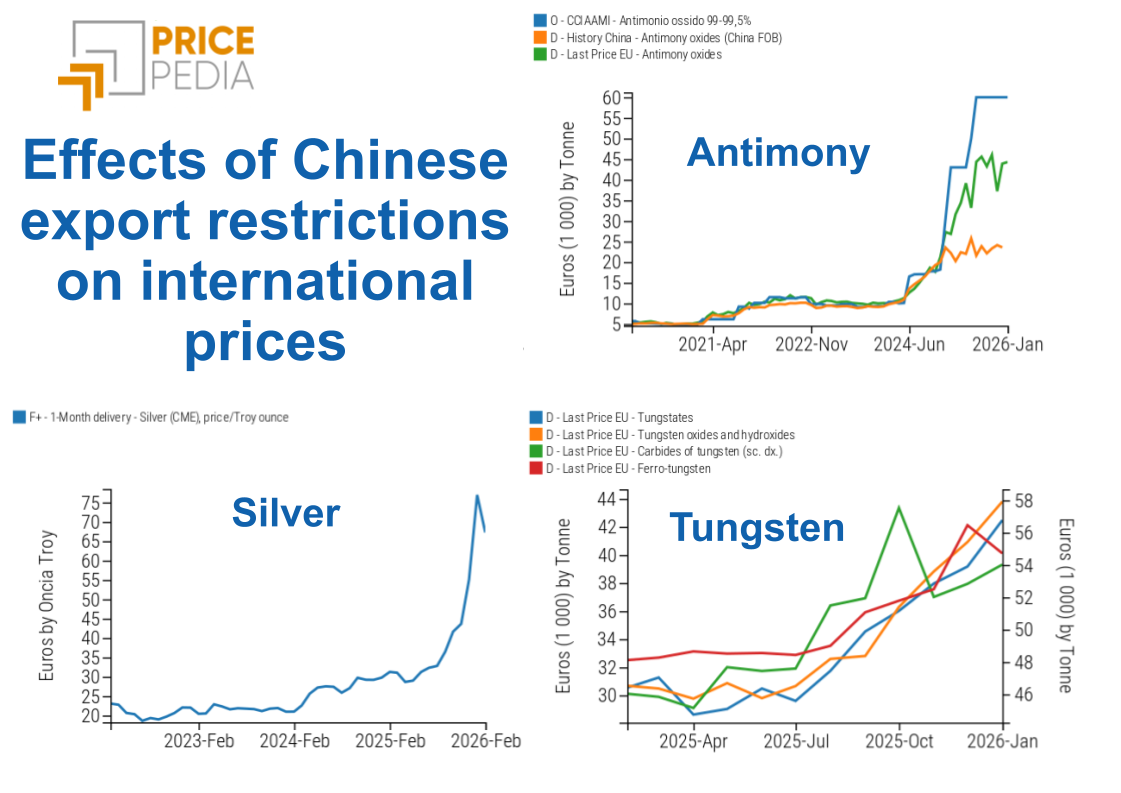

Analysis of European prices in the tungsten supply chain

The chart below shows the historical series of various EU customs prices of tungsten, expressed in euros per ton.

Historical series of EU customs prices of tungsten, expressed in euros per ton

The analysis of the chart shows a generalized increase in prices across the entire tungsten supply chain, with levels reaching new historical highs. Following the export restrictions introduced by China in February 2025, prices of various European tungsten-based products have more than doubled.

Among the different product categories traded, tungsten carbides recorded the smallest increases, although still showing a significant rise of around 75% between February 2025 and May 2026.

Such price growth dynamics, although particularly pronounced, may still underestimate a tension that is currently confined to the Asian market but could in the future extend to the European market as well.

Do you want to stay up-to-date on commodity market trends?

Sign up for PricePedia newsletter: it's free!

Analysis of Asian prices of ferro-tungsten

The following chart shows the historical series of FOB prices of Chinese exports and CIF prices of Japanese imports of ferro-tungsten, the type of tungsten that has recorded the largest price increase in Asian markets.

Historical series of Chinese and Japanese customs prices of ferro-tungsten, expressed in euros per ton

The chart is “merciless”: starting from February 2025, FOB prices of Chinese exports and CIF prices of Japanese imports of ferro-tungsten have both increased by about six times.

In 2026, China, the main supplier of ferro-tungsten to Japan, following the introduction of new tungsten restrictions, significantly reduced exports of this metal to several countries, including in particular Japan, leading to a substantial supply contraction that was reflected in regional prices.

At present, it is still difficult to determine with certainty whether this tension will remain confined to the Asian market or whether it will also extend to the European one, where prices are “only” about double compared to February 2025 levels. It is evident that the main stabilizing force in the European market lies in a marked contraction in demand, made possible by the substitutability of tungsten with other metals, particularly molybdenum in some special steel applications.

Conclusions

Tungsten is a critical commodity for several countries around the world, whose supply depends largely on Chinese shipments. The new constraints introduced by China on tungsten exports have therefore led to a sharp increase in international prices, with dynamics that are however significantly different between the European and Asian markets.

Currently, both FOB prices of Chinese exports and CIF prices of Japanese imports, recorded from two independent customs sources, indicate ferro-tungsten price levels about six times higher than February 2025 levels, the month in which the first export restrictions were introduced by China. In Europe, instead, the price increase has been much more limited, with values roughly doubled compared to February 2025.

It is difficult to determine whether the anomalous growth observed in Chinese and Japanese markets will remain confined to Asian regional contexts or whether it will also spread to European price dynamics. The evolution will largely depend on the actual substitutability of tungsten with other metals, especially in the steel sector. What is evident, however, is the marked vulnerability of the European supply chain, which is highly dependent on the Chinese market for tungsten procurement—a factor that represents a potential risk for market stability.

For this reason, the European Union is strengthening its raw material security policies under the Critical Raw Materials Act, aiming to diversify supply sources, reduce dependence on single suppliers, and increase supply chain resilience. In this context, the EU is developing a coordinated initiative for the creation of strategic stocks of critical raw materials. Among the materials identified for the first storage schemes is tungsten, along with other strategic minerals such as rare earths and gallium, with the goal of further strengthening supply security and reducing dependence on China.

[1] Source: U.S. Geological Survey (USGS): Mineral Commodity Summaries 2025.

You may be interested in:

China's rise in the critical commodities market: industrial strategies and geopolitical levers

Published by Luca Sazzini. .

Terre rare Antimony Tungsten Critical raw materialsHow did China become the global leader in critical commodities? [ Read all ]

Tungsten, antimony and silver: what do they have in common?

Published by Luigi Bidoia. .

Precious Metals Antimony Tungsten Critical raw materialsLa limitazione delle esportazioni cinesi porta i prezzi mondiali alle stelle [ Read all ]

How the Chinese market influences the EU market: the case of tungsten and its compounds

Published by Luigi Bidoia. .

Energy Transition Tungsten Critical raw materialsIl composto più importante sono i carburi di tungsteno, il cui prezzo in Europa è determinato dai prezzi cinesi via costi [ Read all ]