The great speculation

The opportunities for speculating on the prices of basic chemicals have never been so high

Published by Luigi Bidoia. .

Conjunctural Indicators Organic Chemicals Global Economic TrendsThe current market anomaly

One of the cornerstones of economic theory is the strong relationship between average production costs and sales prices. Depending on the form of the market, this relationship can result in a share or an equality, generating in the first case extra-profits. This relationship, however, takes time, generally not a short one, to come to fruition. In the short term, however, there may be situations in which there does not seem to be any relationship between average prices and costs. This appears to be the case in many commodity markets in Europe since the start of the pandemic until today.

The possibility of a short-term misalignment between average costs and prices creates the conditions for speculative behavior to increase. This statement requires us to define what is meant by speculative behavior and, above all, what are the effects, positive or negative, that they can have on the functioning of the markets. The most consolidated definition is that given by Nicholas Kaldor in one of his essays from 1939: "buying (or selling) goods with the prospect of selling (or buying) at a later date, having as a reason the expectation of a change in prices". At the basis of the speculative behavior there is therefore the expectation of future changes in the prices of the asset involved in the transaction.

Effects of speculation on the functioning of markets

A heated debate characterized the judgment on the effects of speculation. At one extreme are those who, following Einaudi's footsteps, believe that speculative behavior is positive for the economic system because they allow those who want to hedge themselves (the hedgers) to transfer to other subjects (the speculators ) the risk linked to uncertainty about the future. At the opposite extreme are those who see the dangers due to the existence of "noise traders", ie poorly informed operators who are moved by imitative behaviors rather than by rational evaluations. A significant presence of these operators can lead to such high price volatility as to expel rational operators from the market, adding uncertainty to the natural formation of prices.

The potentially negative aspects due to the existence of noise traders are largely increased by the possibility

that information on the markets is manipulated by interest groups, orienting prices in the desired direction.

Real market speculation

Since the postwar period, much of the speculative behavior has occurred in the financial markets and the real estate market. Historically, they have also often concerned real markets for raw materials and basic intermediate goods, producing case studies that are rich in economic history. Among the best known, the cotton famine (The Lancashire Cotton Famine) which hit the English cotton industry due to the blocking of imports of raw materials from the Southern Confederate States during the American Civil War (1861-1865) and the hoarding by English traders.

Documented cases on real markets have always involved relatively isolated speculations. They have never concerned a high multiplicity of products at the same time, as is the current case on the European basic chemicals market.

As often happens on real markets, speculative behaviors are mainly carried out by distributors who have fewer relationship ties with end users. A possible measure of the effects of these behaviors can be obtained from the comparison between the prices recorded at customs, the result of transactions between operators with similar bargaining power, and the prices recorded through panels (in this case of the Milan Chamber of Commerce) of specialized operators who generally, they report prices relating to transactions between distributors and end users.

Using this methodology, in the next part we will measure the intensity of these behaviors on the European market for basic organic chemistry goods. We will first analyze the prices of two spirits; then that of four organic acids and finally the prices of two acetates.

Speculation on the alcohol markets

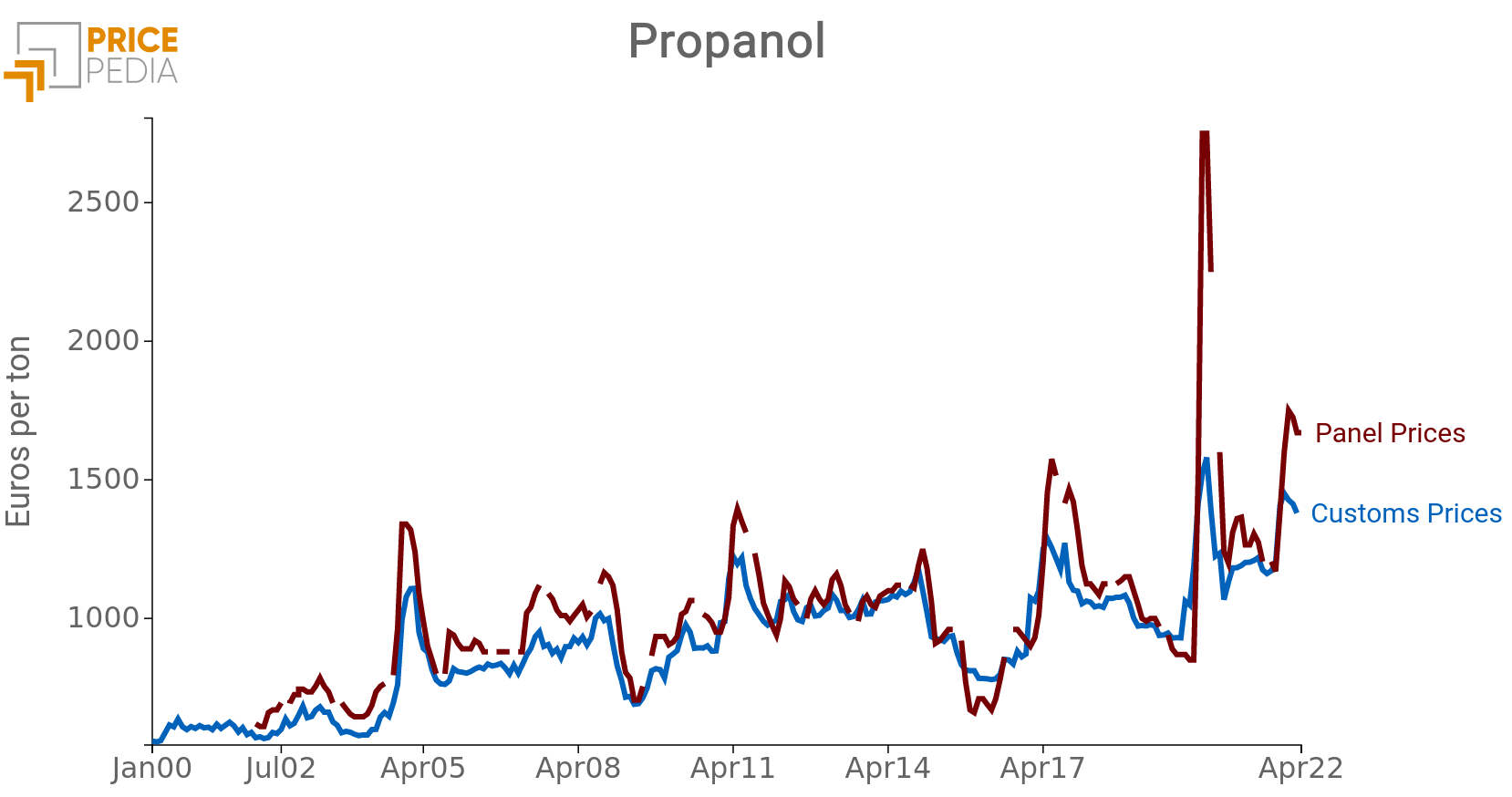

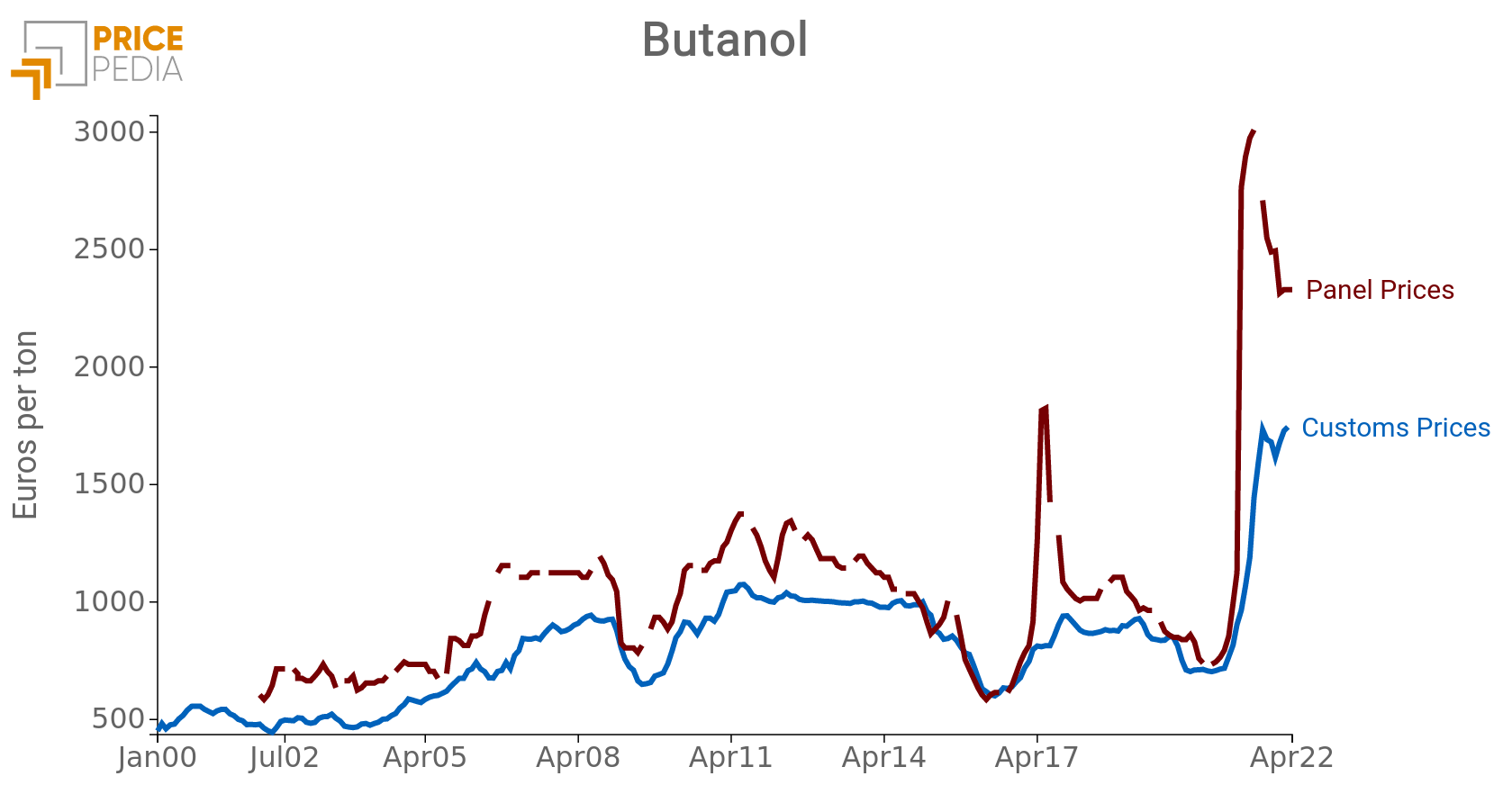

The following graphs show the comparison between the customs price and the panel price of two alcohols: Propanol (or n-propyl alcohol) and Butanol (or n-butyl alcohol).

Alcohol price (euro per ton)

|

|

From the analysis of these graphs, it is clear that there was an attempt to manipulate market information on Propanol prices as early as the spring of 2020, when the news of possible large increases in the worldwide consumption of isopropyl alcohol began to circulate, as a hand sanitizer. In just a few months, price declarations rose from less than € 1,000 per ton to almost € 3,000. The speculation was not successful, however, and by the end of the year the declarations had returned to around 1000 euros per ton. In the first months of the pandemic, customs prices also increased significantly, supported by the strong increase in world demand, but the maximum level reached was only 1500 euros/ton.

The attempts at speculation on Butanol are more recent, relating to spring 2021, when the price requests reported by the panel went from less than 1000 euros to almost 3000 euros per ton in a few months. Also in this case the prices initially requested were not accepted by the market and in the following months they fell back towards 2000 euros. At the same time, customs prices have registered a phase of significant growth since the beginning of 2021 and then stabilized in recent months at a level close to 1700 euros.

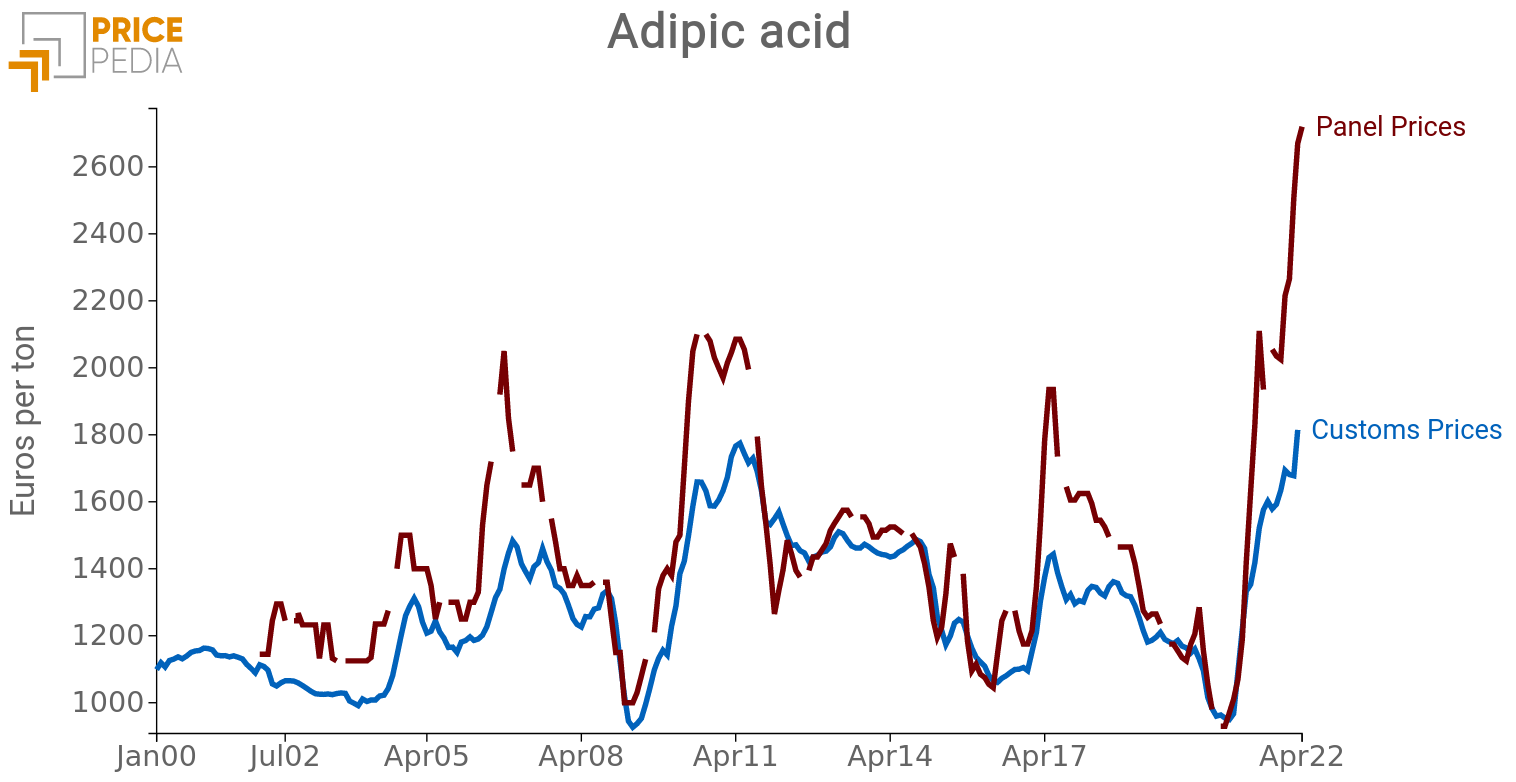

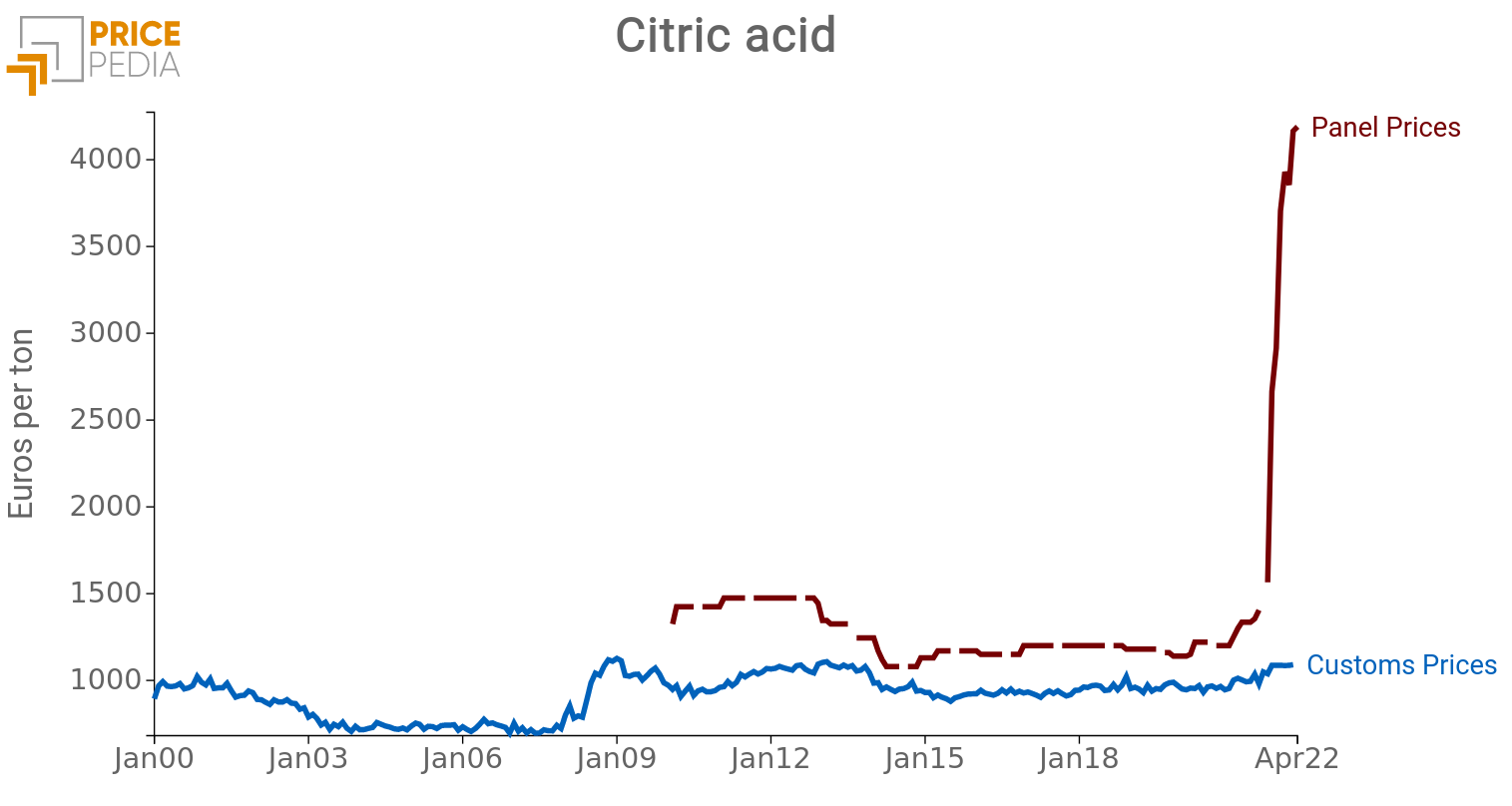

Speculations on the organic acid markets

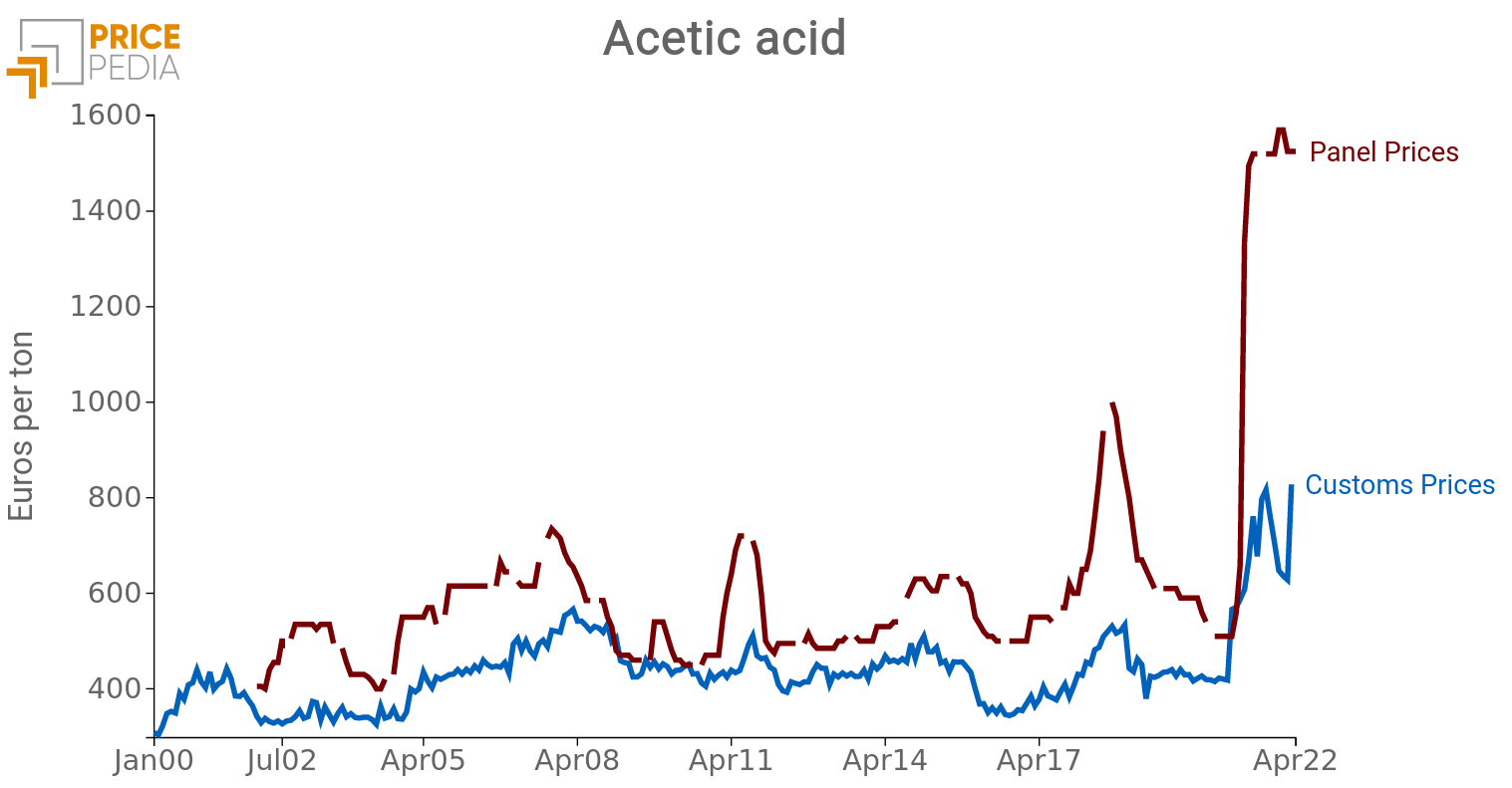

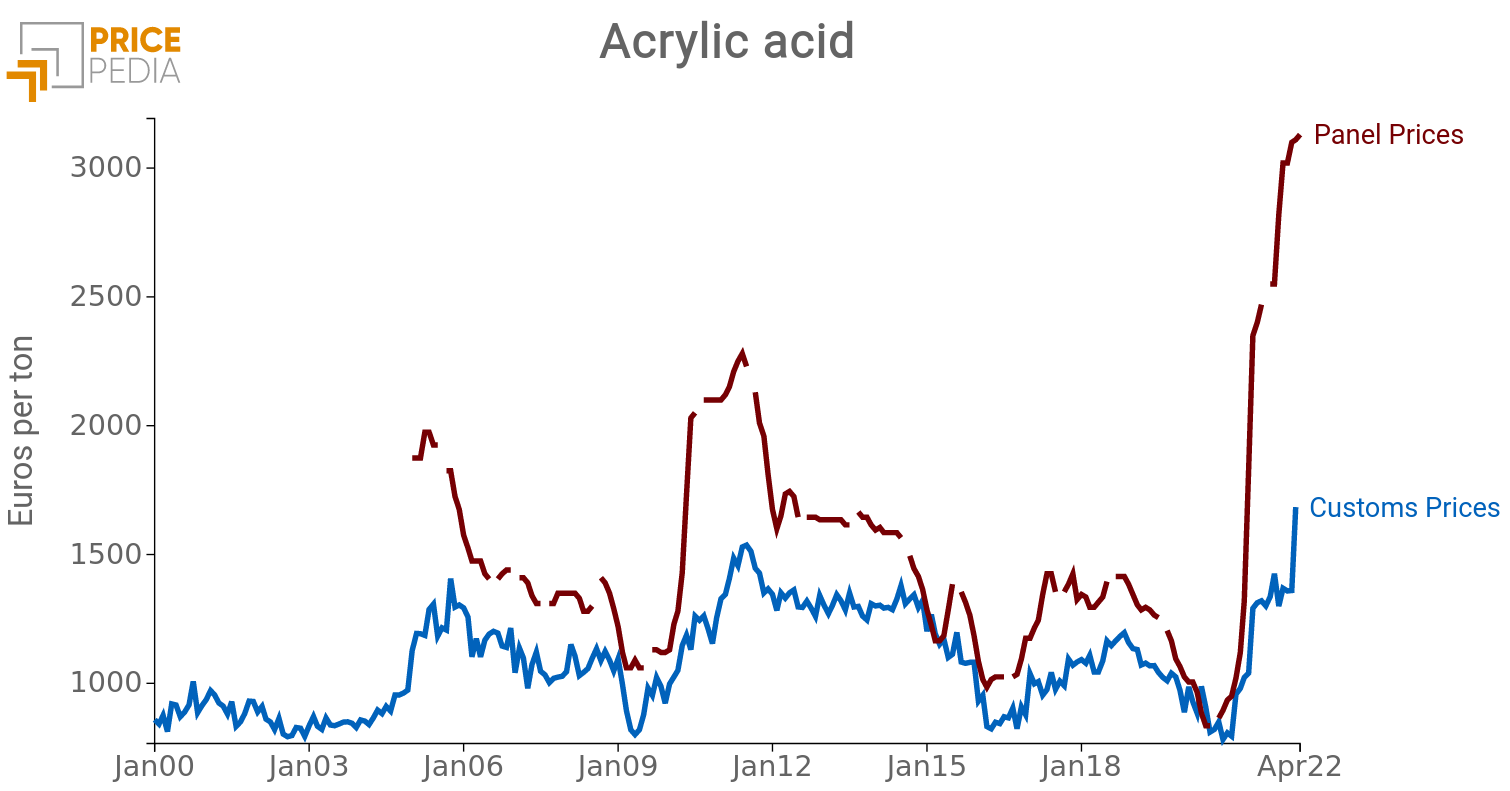

The four graphs shown below show how speculative behavior is currently characterizing the price of organic acids.

Organic acids price (euro per ton)

|

|

|

|

For the price of acrylic acid and adipic acid, the start of the growth phase took place between the end of 2020 and the beginning of 2021. This growth it continued in the following months until it exceeded, in the prices declared by the panel, 2600 euros for adipic acid and 3000 for acriclic acid.

More recent, and more concentrated over time, was the increase recorded by acetic acid. In panel prices, in just one month (April 2021), it went from 660 euros / ton to over 1300 euros.

Even more recent and very intense is the growth in the panel price of citric acid, which went from € 1350 / ton in June 2021 to the current 4200.

These increases are matched by parallel increases in customs prices, the intensity of which is however much lower. The resulting picture is the existence of market factors that lead to a generalized rise in the price of organic acids. These factors, however, were such as to justify increases, in annual terms, of the order of 40-60%, and not more than 100% as shown by the panel prices, with a peak that exceeds 200% for acid. citric.

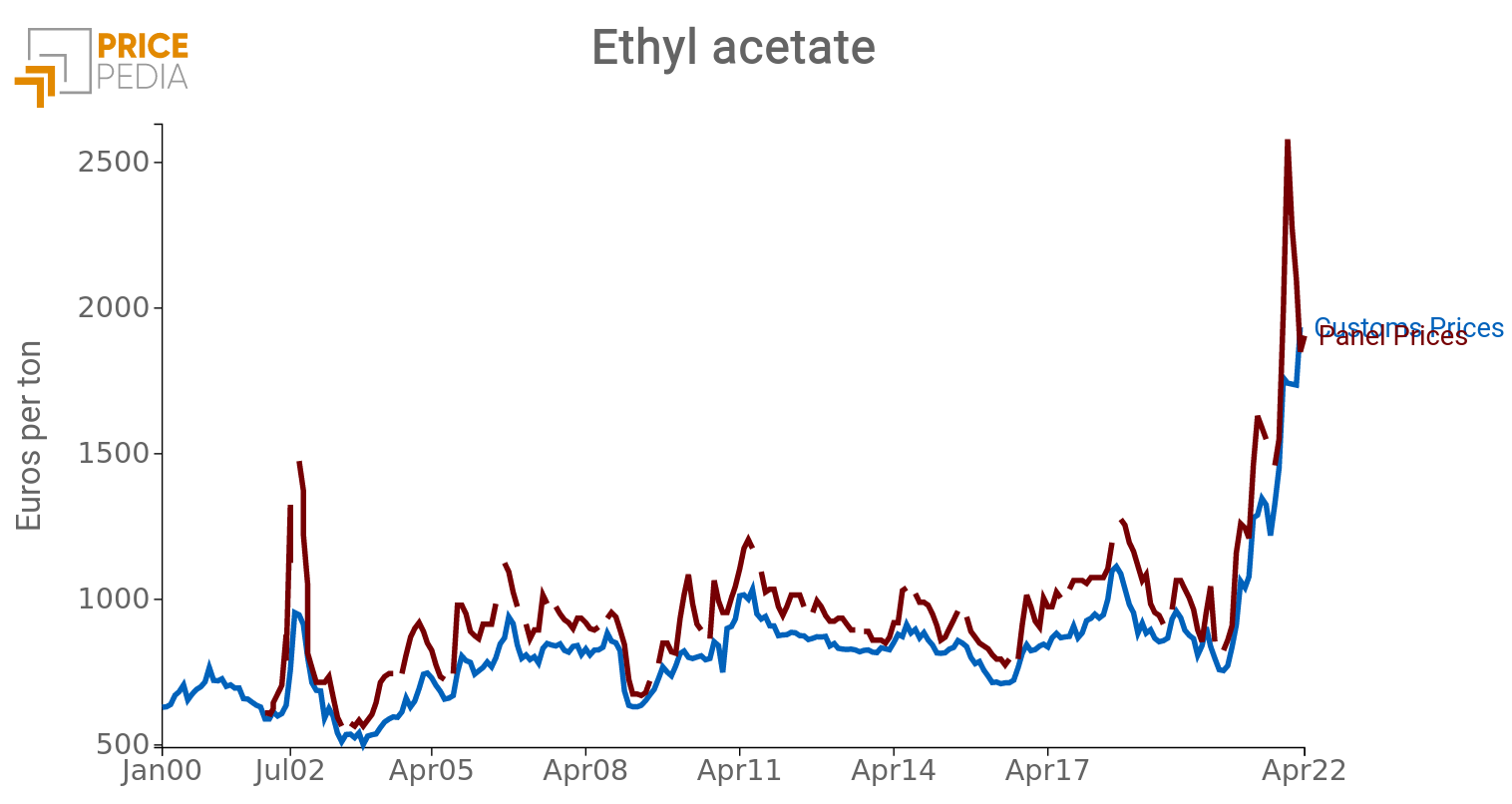

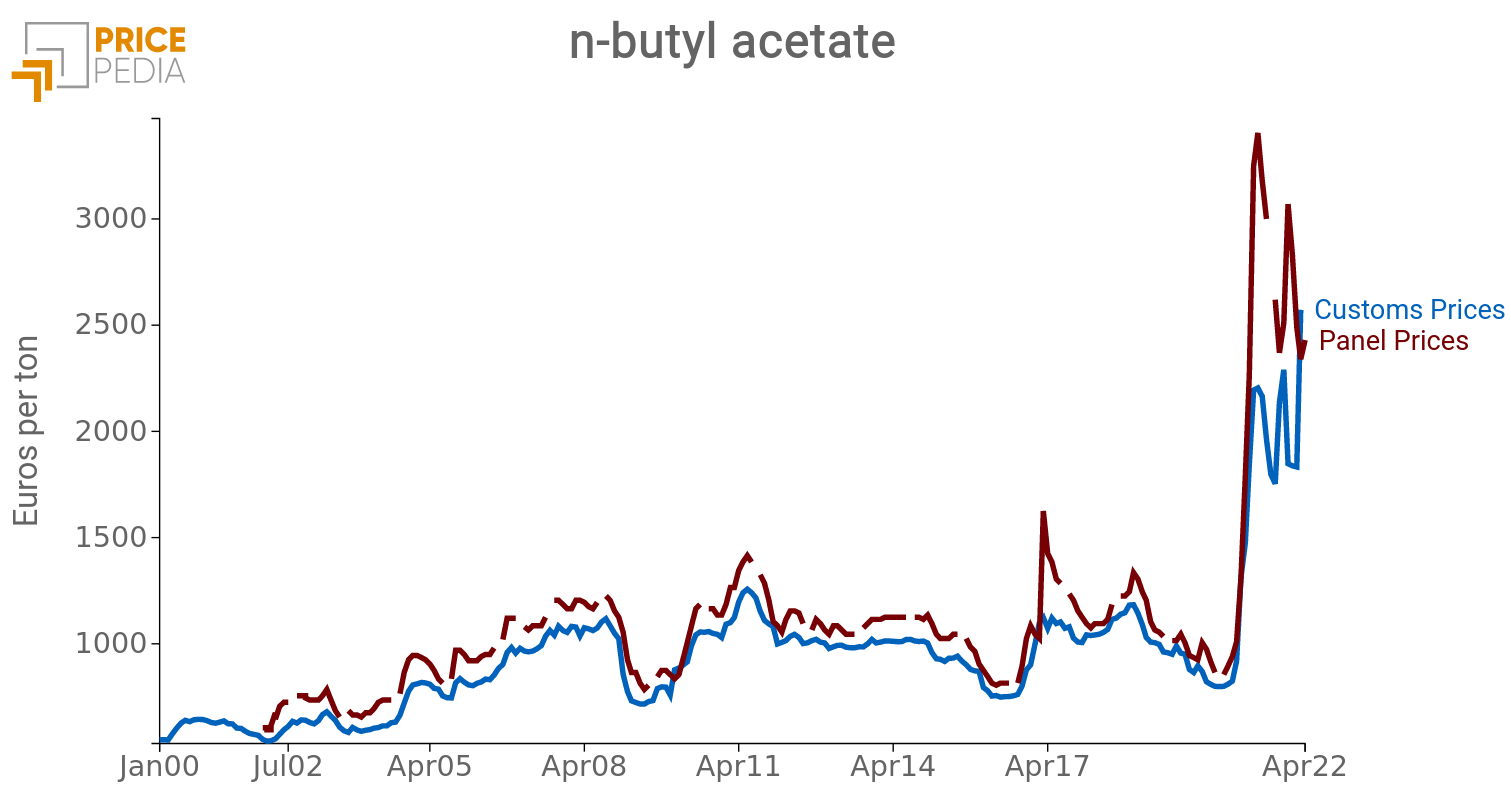

Speculations on the acetate markets

Below is the comparison between the dynamics and price levels of two acetates: ethyl acetate and n-butyl acetate.

Acetate price (euro per ton)

|

|

The analysis of these two graphs clearly shows the phase of strong growth that has characterized the prices of these two acetates since the beginning of 2021, recorded uniformly by panel prices and customs prices.

However, while the growth in customs prices stopped at the end of 2021, that of panel prices continued to exceed € 2,500 for

ethyl acetate and € 3,000 for n-butyl acetate. However, the attempt to influence the market by manipulating price information does not appear to have been successful. In recent months, panel prices have plummeted for both acetates, aligning perfectly with customs prices.

Conclusions

The comparison between the prices declared by a panel of specialists (probably also concerning price requests and not only actual prices) and customs prices (certainly more corresponding to actual market transactions) allows us to document how more phases of speculative behavior on the prices of basic organic chemicals. Currently these seem to have returned in the case of alcohols and acetates, while they remain particularly intense in the case of acids.

You may be interested in:

Analysis of financial commodity prices amid supply imbalances and tensions

Published by Luca Sazzini. .

Conjunctural Indicators Commodities Financial WeekCommodity markets continue to be marked by high uncertainty [ Read all ]

China economic update May 2026

Published by Luca Sazzini. .

Conjunctural Indicators Global Economic TrendsFOB prices for Chinese commodity exports continue to rise [ Read all ]

Downward pressure on the financial markets for commodities

Published by Luca Sazzini. .

Conjunctural Indicators Commodities Financial WeekWhat factors are driving commodity price trends? [ Read all ]