Building a reliable should cost: the importance of breakdown analysis

With the new PricePedia feature, technical cost analysis becomes simpler, more accurate, and automated

Published by Luca Surace. .

Strumenti Should Cost The should cost, i.e. the technical reference cost of a purchased good, is a fundamental tool for the purchasing department, both in budget definition and in improving negotiations with suppliers.

When dealing with a composite good, it is not easy to identify reliable forecast scenarios that indicate to the purchasing department the likely price evolution during the budget year. However, it is often possible to obtain more precise information on the price trends of the inputs required for its production.

To translate this information into a concrete indication of the finished good's price, the most useful tool is precisely the should cost, which aggregates the forecasted prices of the inputs into an overall technical cost (thus excluding suppliers' commercial policies).

Knowing the past and future dynamics of the technical cost of the purchased good also represents a competitive advantage towards the supplier: the purchasing department can bring this information to the negotiation table, making the discussion more transparent, reducing the time needed to define the price, and freeing up resources to focus on other aspects of the purchase, often sources of win-win solutions.

The breakdown analysis

One of the activities that most often makes the construction of a should cost complex is the breakdown (or decomposition) analysis of the good's total cost into its cost components. This phase is fundamental and preliminary to the calculation of the should cost and involves the following steps:

- choosing the technical coefficients reference base;

- identifying cost components and calculating their technical coefficients;

- valuing each component and calculating their cost incidence.

1. Technical coefficients reference base

The technical coefficients, which express the required quantity of each input, can be calculated with reference to one unit of the final good or to its total weight.

If the reference base is one unit of the good (for example, an electric motor), the technical coefficients will indicate how much of each input is needed to produce a single unit of the good.

If instead the base is a weight quantity (for example, one ton of electric cables), the technical coefficients will express the quantity of each input required to produce one ton of the finished good.

2. Calculation of the individual components' cost coefficients

This phase involves identifying the input factors required for the production of the good and measuring their technical coefficients, i.e. the quantities of input needed to obtain a certain quantity of output.

As previously seen, the output can be expressed in units or weight.

The measurement units of the inputs vary based on their nature. In most cases, the most common unit is weight. In these cases, the technical coefficient will be expressed, for example, in kilograms per ton or in kilograms per unit of finished product, depending on the reference base.

However, there are inputs for which the technical coefficient cannot be expressed in weight. This is the case, for example, of electricity or gas used for heat production. In these cases, the most appropriate unit of measurement is KWh, always calculated in relation to the reference base (weight unit or product unit).

Another case concerns the services necessary for the realization of the finished good. Here, the most appropriate unit of measurement is the value of the service, related to the obtained product quantity (by weight or unit).

Similar to services is the input represented by labor, which should be expressed in value per unit of weight produced or per single good. For labor, determining the value per unit of output is simpler, since it can be calculated by considering the hours used for production, multiplied by the average hourly cost of the involved workforce.

3. Calculation of cost incidences

Once the technical coefficients for each production input have been calculated, they must be valued using the price of each input at a specific date (for example, January 2022). The sum of the values of all inputs allows determining the total production cost of the good and, subsequently, the percentage cost incidence of each input, given by the ratio between the cost of the individual input and the total production cost.

Once the cost incidences of the various inputs are known, the should cost can be calculated by aggregating the price indices of the different inputs, weighted according to their incidence on the total cost.

Integration of breakdown analysis into PricePedia’s Should Cost functionality

Among the features available on the PricePedia platform is the should cost, which until recently allowed the calculation of the technical cost of a product through the user's manual entry of input components and their respective cost incidences.

In the version released this week, the user can continue to calculate the should cost by directly entering the cost incidences of the various inputs, or – if preferred – can enter the technical coefficients, letting the platform automatically convert them into their respective cost incidences.

In summary

The should cost is a powerful tool available to purchasing departments. In the version of PricePedia released today, the user can use the should cost functionality in two ways:

- by directly entering the cost incidences of the various input factors;

- by entering the technical coefficients and letting the system automatically calculate their respective cost incidences.

The ability to build the should cost starting from the technical coefficients of the various cost factors allows for significant time savings and reduces the risk of calculation errors.

You may be interested in:

The arrival of foundation models in time series forecasting

Published by Riccardo Gentilucci. .

Strumenti Machine learning and EconometricsNew Machine Learning Forecasting Systems [ Read all ]

Tokens & Transformers: the heart of modern Machine Learning models

Published by Luigi Bidoia. .

Strumenti Machine learning and EconometricsCome una tecnologia unificata ha accelerato l’evoluzione dell’AI [ Read all ]

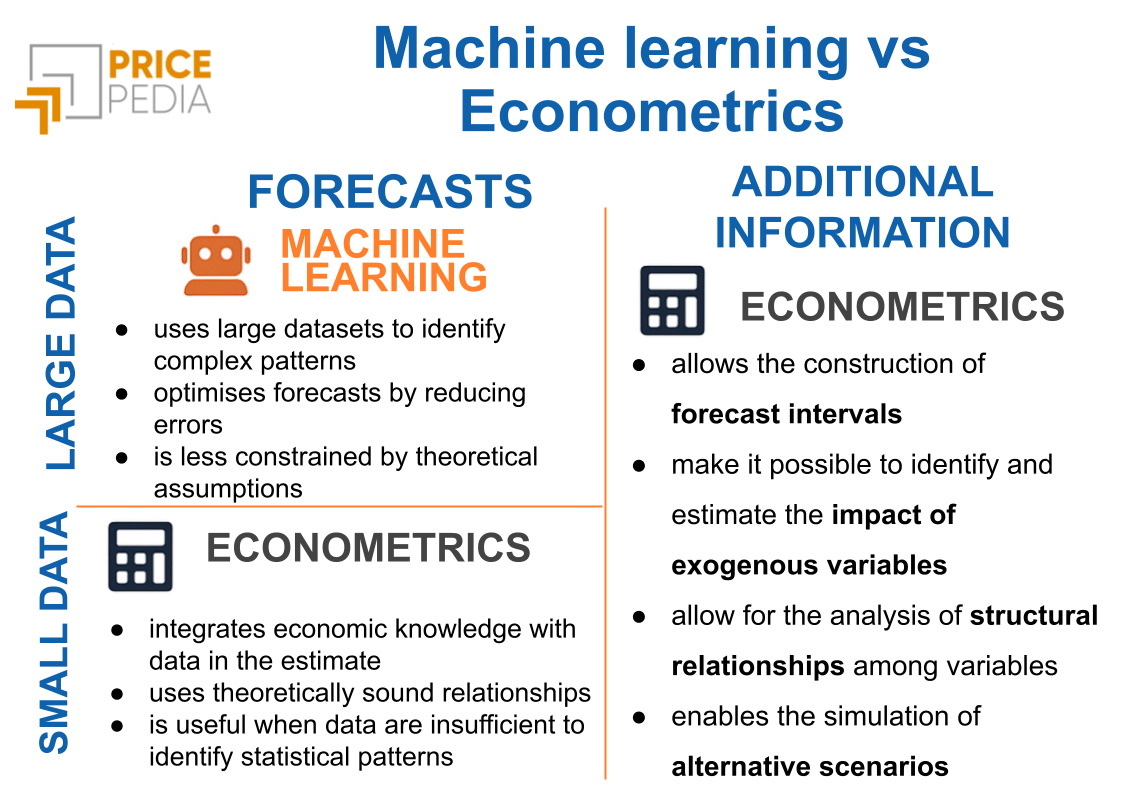

Machine Learning and Econometrics: Alternative or Complementary Tools?

Published by Luigi Bidoia. .

Strumenti Machine learning and EconometricsIl Machine Learning potrà sostituire l’econometria nelle previsioni, ma non nell’analisi e nella comprensione delle cause di un fenomeno [ Read all ]