Back to growth: an uncertain scenario

Doctor Copper Says: copper price dynamics to monitor the economy

Published by Alba Di Rosa. .

LME Copper Non Ferrous Metals Macroeconomics Doctor Copper SaysThe price of copper confirms its relative stability amid uncertainty in recent days. Compared to last week's closing values, we can see a modest 1 percent decline on both the London Metal Exchange (LME), closed today in view of the Easter holiday, and the Shanghai Futures Exchange (SHFE).

Among the news that caused quite a stir this week in the world of commodities, we can find the surprise announcement by OPEC+ last Sunday that it plans to cut oil production by more than 1 million barrels per day, from May until the end of the year.

Both WTI and Brent prices have reacted upward since Friday's March 31 close, reflecting an increase in markets' perception of risk. Thus, concerns about inflationary pressures, and related monetary policy choices, are strengthening, due to their potential impact on global economic growth.

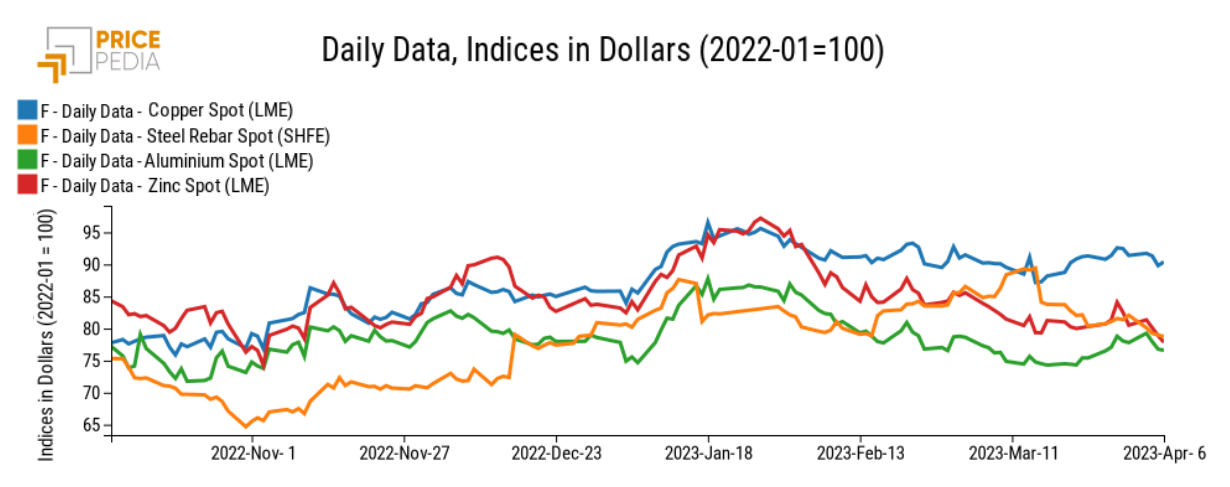

As we approach the Easter break, markets therefore seem to be closing on a lack of particular optimism, as confirmed by metals prices: after a rise in early 2023, linked to hopes about Chinese reopenings, there have been no signs of a clear acceleration in recent months, as can be seen from the chart below. Among the various metals prices, copper seems to stand out as fairly resilient, supported according to Fitch by strong market fundamentals.

Manufacturing sector: a focus on US and China

Looking at the latest data on the health of the manufacturing sector, news from the US and China this week weighed, in turn, on market sentiment, and indirectly on the price of copper as well.

The Institute for Supply Management recently released the US manufacturing PMI for March.The survey signals that US manufacturing activity showed signs of contraction in March, for the fifth consecutive month, after a 28-month period of growth. The index marked 46.3, below the neutral threshold of 50.

Thus, we can see the effects of a tightening monetary policy on the economic slowdown, as well as the impact of inflation on purchasing power.

Looking instead at the Chinese case, after the solid growth in manufacturing output and new orders recorded in February, there come signs of stability at the end of the first quarter. For the month of March, the Caixin China General Manufacturing PMI in fact stood at the neutral level of 50, down from the high of the past 8 months touched in February.

Primarily holding back the PMI we can find a smaller increase in terms of manufacturing output; total new orders also increased at a more moderate pace. While some companies reported that demand and customer numbers improved due to the recent easing of pandemic measures, others reported relatively weak sales, especially overseas. China's PMI thus signals the risk of a foreign demand slowdown, which for the time being seems to be weighing mainly on small businesses.

In contrast, the services PMI for China in March confirmed a growth trend, in line with the dynamics of the Eurozone.

“So far, we have proven to be resilient climbers. But the path ahead—and especially the path back to robust growth—is rough and foggy”

At the close of the first quarter of 2023, the world economy thus confirms a challenging scenario. According to the latest statements by Kristalina Georgieva, Managing Director of the International Monetary Fund, ahead of next week's release of the World Economic Outlook, the Fund expects the world economy to grow by less than 3 percent this year: this growth rate can be considered as weak compared to the historical average; India and China will contribute positively, while the outlook for the United States and the Eurozone is less optimistic.

You may be interested in:

PricePedia scenario for non-ferrous metals 2026-2027

Published by Luca Sazzini. .

Forecast Non Ferrous Metals ForecastWhat impact did the Persian Gulf war have on PricePedia’s forecasts for non-ferrous metals? [ Read all ]

From ore to metal: what explains the recent price divergence in the lead market?

Published by Luca Sazzini. .

Non Ferrous Metals Lead Price DriversComparison between the prices of minerals and related raw metals [ Read all ]

Tin under pressure: decline in Indonesian supply pushes prices up

Published by Luca Sazzini. .

Tin Non Ferrous Metals Price DriversIndonesia: hub of global tin supply [ Read all ]