Effect of stocks on the prices of basic goods

Between late 2021 and early 2022, the European economy accumulated stocks like never before

Published by Luigi Bidoia. .

Last Price Conjunctural Indicators Global Economic TrendsIn the recovery phase of the activity levels of world industrial production after the first wave of Covid19, the increase in inventories in upstream and downstream warehouses was one of the factors that contributed to significantly increase the demand for raw materials and basic goods.

Corporate purchasing policies

In fact, during 2021, all the factors that influence the purchasing policies of the companies were found to support the increase in inventories:

- Demand expectations: the speed with which the recovery of world industrial production took place in the second half of 2020, supported by high public interventions in support of growth, led economic operators to extrapolate the growth underway also in the near future. As long as inflation, conflict in Ukraine, zero-covid policy and related lockdowns in China, changes in economic policy in the US and the EU, did not reverse expectations, the expectations of companies were for a prolonged phase of world economic growth.

- Expected prices: in 2021, expectations on price changes were marked by generalized growth. Under normal conditions, this leads companies to anticipate increases by accumulating inventory.

- Cost of money: in 2021 the average rate on bank loans to companies for working capital transactions was 2.9% compared to an average rate of 3.1% in 2019. At the lowest cost of money In addition, it is easier for companies to obtain credit, thanks to massive injections of liquidity in the US and the EU and government support measures, especially in terms of guarantees.

- Increase in delivery times: the difficulties of logistics both internationally and locally have resulted in a general increase in delivery times. In this situation, the primary objective of the companies was to guarantee the availability of production inputs, increasing the volumes of purchases.

The effects on company inventory volumes

All these factors in 2021 have, therefore, supported the purchasing policies of companies, leading some analysts to speak of a generalized situation of overbought.

Confirmation of the effects of the increased purchases on the inventories of manufacturing companies is given by the Intesa-SanPaolo internal survey of November-December 2021 on the behavior of client companies (see this report [only in Italian]).

This survey shows that almost all Intesa San Paolo client companies, during 2021, increased the volume of raw materials and semi-finished goods warehouses. Furthermore, a good majority of companies have increased their stocks of finished products in order to satisfy any sudden acceleration in demand.

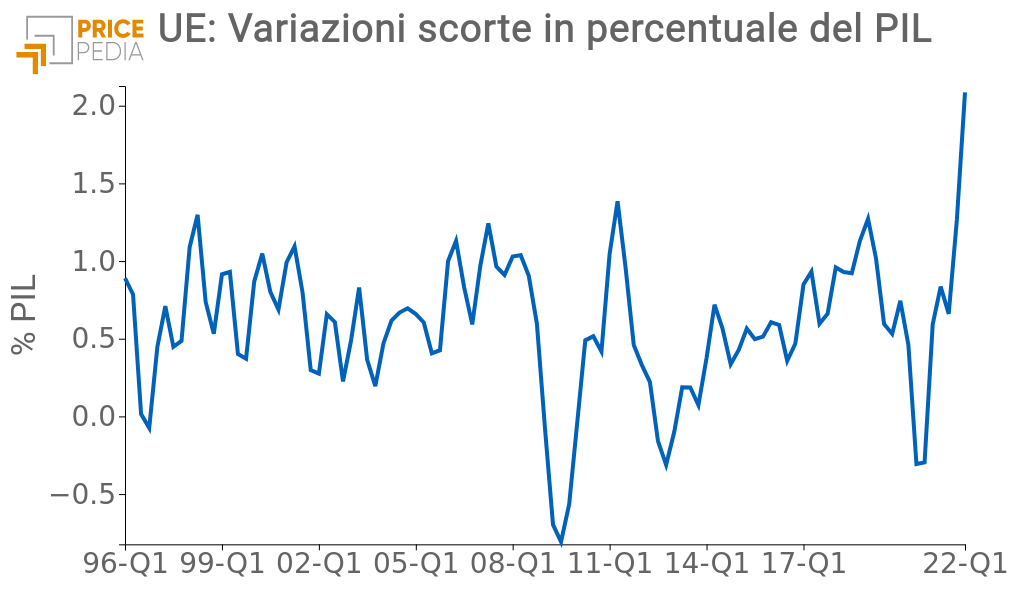

A measure of the intensity of stock accumulation by European companies can be obtained from the national accounts of EU countries, by comparing the changes in stocks in the different quarters with the GDP created in the same period. The graph shows the quarterly historical series of the indicator just described for the whole of the 27 EU countries, from the first quarter of 1996 to the first quarter of 2022.

As can be clearly seen from the graph, the six months ending with the first quarter of 2022 turn out to be an outlier of the historical series of changes in stocks as a percentage of GDP. In fact, in the six months from 1 October 2021 to 31 March 2022, European companies increased their stocks in upstream and downstream warehouses for a value equal to 2% of the gross domestic product created in the corresponding 6 months, leading to an accumulation never first recorded in the history of the last 25 years. The maximum accumulation, prior to the current one, was recorded in the first half of 2011, when the indicator touched 1.4% of the GDP generated in the corresponding half year.

A further significant accumulation is likely to have occurred in the second quarter of this year, leading to a significant change in corporate purchasing policies. This change will find support in the disappearance of the factors that had, conversely, supported the replenishment of stocks in 2021 and in the first months of 2022.

Demand expectations are less and less optimistic, as the various surveys on businesses indicate; commodity prices are falling not only on financial markets but also on real markets; the cost of borrowing is rising and banks' lending policies are becoming more restrictive.

The only factor that could still sustain high stock levels is the long lead times.

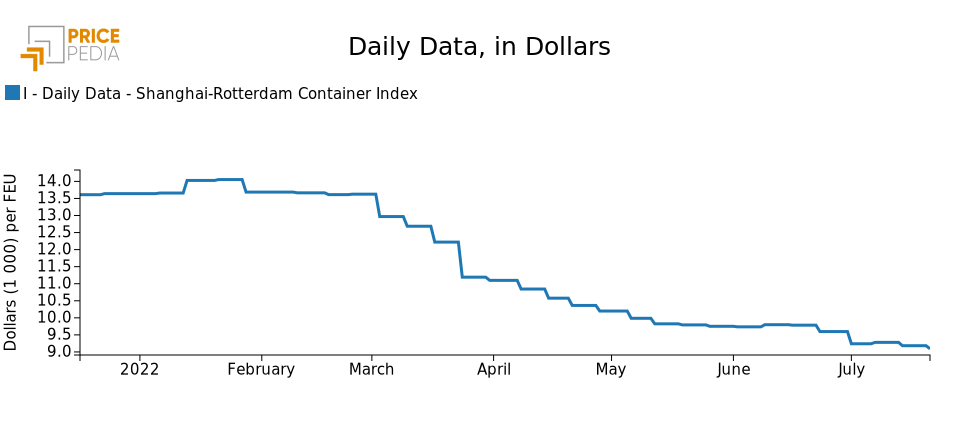

Even in this area, however, the situation is rapidly changing, as is reported by the price of the freight of a FEU from Shanghai to Rotterdam. We are still a long way from pre-pandemic values, but the freight of this route, representative of world trade, has dropped from the maximum of $ 14,000 per FEU (40-foot equivalent unit) at the end of January 2022 to the current $ 9,000.

Ship charter of a FEU on the Shanghai-Rotterdam route

First effects on the prices of raw materials and basic goods

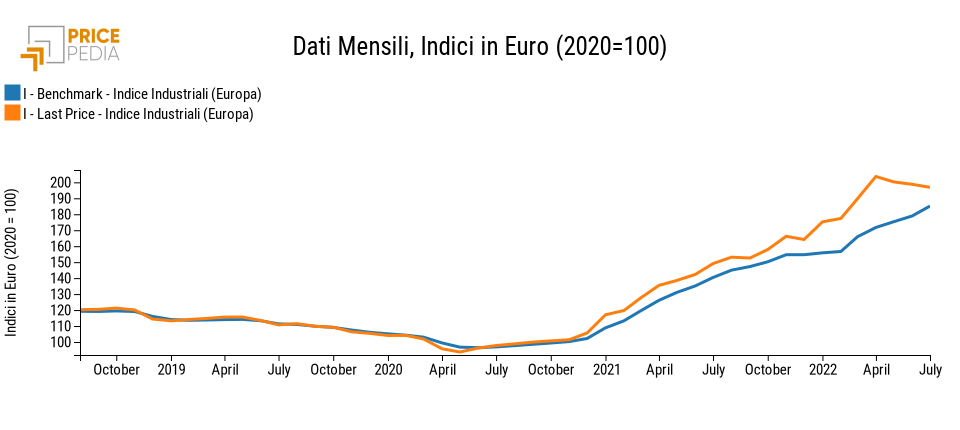

PricePedia recently developed the new Last Price measure (see PricePedia Last Price), obtained from customs prices with the aim of measuring the price of contracts stipulated in the same month in which the goods cross the border. The graph below shows the comparison between the Last Price index and the traditional Benchmark index for all raw materials and basic industrial goods (therefore excluding energy and food), calculated simply by considering the average prices of all goods that have passed through customs in a given month.

EU price index of industrial commodities: comparison between Last Price and the base customs price (Benchmark)

As is clear from the graph, while the Benchmark measure also increased in July (due to the effect of contracts signed in previous months), the Last Price measure recorded a decrease in the last three months. The decrease is very limited, close to -1% monthly, but the signal that a reversal of the cycle of industrial commodity prices is taking place in the real European markets is clear and robust.

Conclusions

The analysis described above leads us to believe that in the coming months the demand for industrial commodities on the European market could record a significant decrease, not so much due to a decrease in industrial activity levels, but due to a significant change in the purchasing policies of companies along the various production chains. In this situation, the uncertainty is not so much about the direction that industrial commodity prices will take, but about the intensity of the decrease.

Do you want to stay up-to-date on commodity Market trends?

PricePedia Newsletter: sign up!

You may be interested in:

The latest escalation in the Middle East is reigniting tensions in the commodity markets

Published by Luca Sazzini. .

Conjunctural Indicators Commodities Financial WeekRussia imposes a temporary ban on diesel exports in July [ Read all ]

Analysis of financial commodity prices amid supply imbalances and tensions

Published by Luca Sazzini. .

Conjunctural Indicators Commodities Financial WeekCommodity markets continue to be marked by high uncertainty [ Read all ]

China economic update May 2026

Published by Luca Sazzini. .

Conjunctural Indicators Global Economic TrendsFOB prices for Chinese commodity exports continue to rise [ Read all ]