The Phosphorus Industry: Beyond Fertilizers

An Analysis of Cost Pass-Through Intensity in the Phosphorus Value Chain

Published by Luigi Bidoia. .

Fertilizers Phosphorus Cost pass-throughPhosphorus is a fundamental chemical element for numerous sectors of modern industry. In addition to its historical and predominant role in the production of fertilizers, it is widely used in the food, pharmaceutical, and detergent industries, as well as in the manufacturing of plastics. More recently, it has gained increasing importance in the field of energy storage, particularly with the development of lithium iron phosphate batteries, which are considered a safer and more thermally stable alternative to traditional lithium-ion batteries.

Cost Pass-Through of Natural Calcium Phosphate Prices

The diagram below illustrates the main industrial phosphorus derivatives and the relationships between phosphorus prices and those of its downstream products. This is a simplified representation, as many of the chemical compounds shown can be produced via alternative synthesis routes. The numerical values indicate the price elasticity of the derivative in response to changes in the price of phosphorus-based inputs.

At the foundation of the phosphorus industry are phosphate rocks, composed primarily of calcium phosphate. From these, elemental phosphorus is obtained and used to produce numerous industrial compounds. One of the main derivatives is phosphorus trichloride, used in the synthesis of fine chemicals, pesticides, plastic additives, and flame retardants. However, the most significant product in terms of volume is phosphoric acid, produced primarily by treating natural phosphates with sulfuric acid. Phosphoric acid serves as the key intermediate from which various industrial value chains emerge, leading to the production of phosphate salts (of calcium, potassium, sodium, etc.), polyphosphates, phosphites, and hypophosphites, each with specific applications in fertilizers, detergents, food products, and battery technology.

The elasticity analysis shown in the map reveals a moderate cost pass-through mechanism between natural phosphates (calcium phosphate) and elemental phosphorus on one side, and sulfuric acid on the other. In contrast, the price pass-through between phosphoric acid and its inorganic salts is particularly strong. For example, the price transmission between phosphoric acid and industrial calcium phosphate is close to 1. This means that a 10% increase in the price of phosphoric acid typically results in a comparable increase in the price of calcium phosphate.

The elasticity between phosphoric acid and polyphosphates is also high (0.79), as polyphosphates are derived through direct chemical reactions and their production cost is strongly influenced by the cost of the acid itself. Conversely, elasticity is lower for phosphites and hypophosphites, due to their greater production complexity, the lower cost share of phosphoric acid in their synthesis, and their higher product differentiation.

Similarly, the relationship between the price of phosphoric acid and that of lithium iron phosphate batteries exhibits very low elasticity. Although the phosphate group is structurally integrated into the cathode material, the impact of phosphoric acid on the final cost of the battery is minimal compared to other, higher-value-added components.

Do you want to stay up-to-date on commodity market trends?

Sign up for PricePedia newsletter: it's free!

Global Production and Trade

The country that plays a leading role in the phosphorus industry is undoubtedly Morocco, thanks to its vast phosphate rock reserves, which account for more than half of global reserves. In terms of mining production, however, Morocco ranks as the second-largest producer globally, significantly behind China, whose output is nearly three times greater. Other major global producers include the United States, Jordan, Russia, Saudi Arabia, Egypt, and Peru[1].

The following four charts highlight the main exporting countries worldwide in the four segments into which the phosphorus industry can be divided:

- Natural calcium phosphates, obtained directly from phosphate rock;

- Phosphoric acid, the intermediate compound from which the various phosphorus value chains originate;

- Phosphorus-based fertilizers, representing the largest category of downstream phosphorus derivatives;

- Other phosphorus-based compounds, which include all non-fertilizer phosphorus products.

Main Exporting Countries in 2024 for Phosphorus Industry Products

| Natural Calcium Phosphates | Phosphoric Acid |

|

|

| Phosphorus-Based Fertilizers | Phosphorus Compounds Other Than Fertilizers |

|

|

The analysis of the four charts clearly reveals the following insights:

- With the exception of China, all major phosphate rock producers have primarily developed the value chain that leads from phosphoric acid to phosphorus-based fertilizers;

- China is the only country with significant phosphate rock extraction that, in addition to developing the fertilizer chain, has also expanded into other branches of the phosphorus industry, achieving undisputed global leadership in those segments.

Conclusions

Phosphorus is a key element in modern industry. Its uses are concentrated in the fertilizer sector, but it also plays an important role in the food, pharmaceutical, detergent, and plastics industries.

In recent years, phosphorus has become increasingly strategic due to its application in electric batteries, particularly as a cathode component in lithium iron phosphate batteries.

Phosphorus mining is distributed among many countries, but Morocco stands out due to its dominant share of global reserves.

Most phosphate rock and phosphoric acid-producing countries have historically focused on the fertilizer value chain. Only China has successfully expanded beyond fertilizers to develop other phosphorus-based industries, achieving global leadership across multiple segments.

[1]: Source: U.S. Geological Survey (USGS): MINERAL COMMODITY SUMMARIES 2025

You may be interested in:

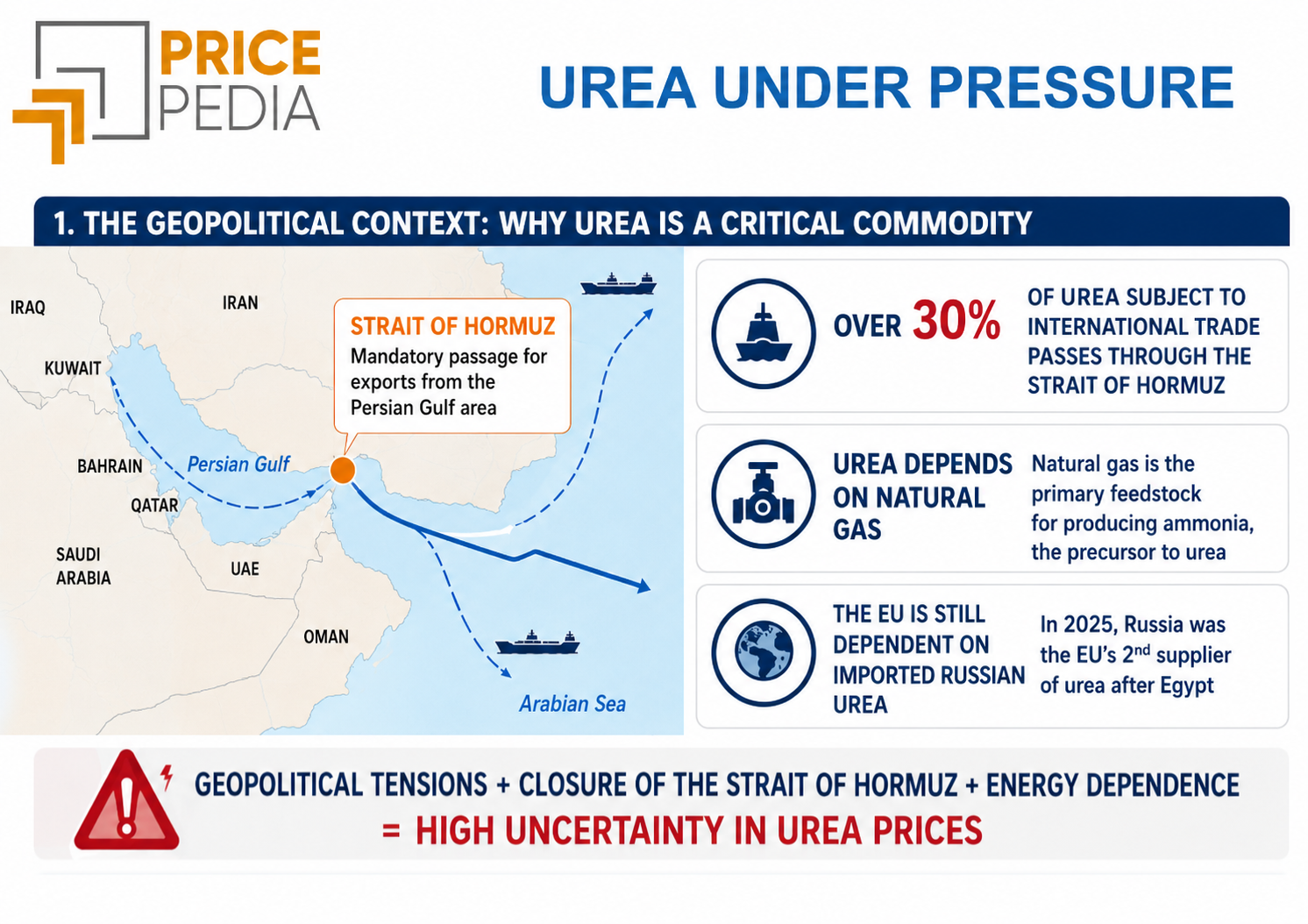

The Importance of Comparisons in Times of High Uncertainty: the Case of Urea

Published by Luigi Bidoia. .

Fertilizers Strait of HormuzL’elevata incertezza attuale rende più difficile interpretare la situazione dei diversi mercati [ Read all ]

How fertilizer prices affect cereal prices

Published by Pasquale Marzano. .

Wheat Fertilizers Price DriversFertilizers are the channel through which the energy shock is transmitted to wheat prices [ Read all ]

Sulfur prices: a new global uptrend cycle?

Published by Luigi Bidoia. .

Fertilizers Sulphuric acid industry Price DriversAfter the peaks of 2008 and 2022, international quotations exceed €250/ton, signaling the start of an intense phase driven by rigid supply and volatile demand [ Read all ]