Criticality analysis of platinum group metals

Importance of PGM metals for European industry

Published by Luca Sazzini. .

Precious Metals Critical raw materialsIn the article Critical Raw Materials: the importance of substitutes, the topic of Critical Raw Materials was introduced, referring to those raw materials deemed "critical" by the European Commission.

The two main parameters for assessing the criticality of a raw material are its economic importance and supply risk.

Economic importance is determined by the number of applications a raw material has within the European industry and its degree of substitutability with other materials.

Supply risk is calculated based on the amount Europe imports from third countries, considering the degree of diversification of the main supplier countries for a specific commodity. The higher the dependence of European imports on a few foreign exporters, the greater the relative supply risk for that particular commodity.

This article delves into the criticality of precious metals belonging to the Platinum Group Metals (PGM), analyzing both the economic importance and supply risk for the European economy. At the end of the article, an analysis of the historical price series of the main precious metals in the PGM category is also provided.

Economic Importance

The Platinum Group Metals (PGM) include six precious metals: platinum, palladium, rhodium, iridium, osmium, and ruthenium. These metals share similar chemical and physical characteristics, as well as having often overlapping industrial applications. Among their main common properties are high catalytic activity, corrosion resistance, high melting points, and excellent conductivity.

The by far most important application of PGM metals is in catalytic converters, where platinum, palladium, and rhodium are essential for reducing hydrocarbon emissions from gasoline and diesel engines. Platinum is mainly used to reduce emissions from diesel engines, palladium for gasoline engine emissions, and rhodium for nitrogen oxide (NOx) emissions. Another significant application is in jewelry, which accounts for about 10% of total PGM consumption.

The chemical industry also registers a strong demand for PGM metals. Platinum is used in oil refining and nitric acid production. Palladium and rhodium are employed in the production of various plastics and polymers, while ruthenium is crucial in ammonia production and, together with iridium, in electrochemical processes.

Other important uses of PGM include:

- electronics: for their conductivity and resistance;

- glass industry: due to their high melting point and corrosion resistance;

- energy technologies: PGM are crucial for fuel cells and hydrogen technologies.

Supply Risk

The criticality of the platinum group metals is mainly due to their economic importance rather than supply risk. However, this does not mean that metals in the PGM category do not pose a supply risk for the EU economy.

To get an idea of how high this risk is, we can analyze European PGM imports from the top 10 exporting countries to the EU.

Main exporters of PGM metals to Europe

The horizontal bar chart above shows that the main exporters of PGM to the EU among non-EU countries are South Africa, the United States, and Russia. Italy ranks third because it re-exports some of the metals previously imported from the United States, South Africa, and Russia.

South Africa and Russia are the two main PGM producers globally. South Africa alone produces 73% of the world's platinum and 39% of the world's palladium. Russia holds 10% of the global platinum production and 38% of the global palladium production.

This means that global PGM production is highly concentrated in just two producer countries, which together hold the majority of the world's production of the two most important PGM metals.

Do you want to stay up-to-date on commodity market trends?

Sign up for PricePedia newsletter: it's free!

Price Analysis

The price analysis of the platinum group metals was conducted only for the three main important metals, namely: platinum, palladium, and rhodium.

The first two are both quoted on the LBMA (London Bullion Market) financial exchange, while rhodium is not quoted on any financial market. For rhodium, the customs prices recorded by the European Union countries were therefore reported.

On the left graph, the financial prices of platinum and palladium from LBMA are shown, while the right graph shows the customs price of rhodium.

| Financial prices of platinum and palladium | European customs prices of rhodium |

|

|

The analysis of the graphs highlights the significant differences between the cycles of the three prices. On one hand, palladium and rhodium prices experienced strong growth in the 2018-2020 triennium due to temporary reductions in global supply. On the other hand, platinum prices have been one of the few commodities to show a substantially flat trend even in recent years.

Until 2017, platinum prices were significantly higher, supported by their use as a catalyst for diesel engines. With 2017, platinum became cheaper than palladium. In those years, there was the diesel emissions scandal in Europe, and the demand for platinum as a catalyst for diesel engines was replaced by the demand for palladium as a catalyst for gasoline engines.

In 2024, the prices of the two metals have returned to similar levels and currently seem to continue following a relatively similar dynamic.

Conclusions

The analysis highlights the high economic importance of the Platinum Group Metals (PGM) for the European economy.

The most important metals within this group are platinum, palladium, and rhodium, mainly used as catalysts to reduce hydrocarbon emissions from diesel and gasoline cars. The production of these metals is highly concentrated in South Africa and Russia, amplifying their supply risk.

Platinum prices have shown a relatively stable trend in recent years, unlike palladium and rhodium, which have just concluded price cycles triggered by a sudden reduction in supply.

For the coming months, we expect an increase in PGM demand until 2025, due to the development of the hydrogen economy and stricter hydrocarbon emission regulations. After 2025, a slowdown in PGM demand is anticipated, driven by the spread of the EV market.

You may be interested in:

Analysis of rhodium's criticality: the world's most expensive precious metal

Published by Luca Sazzini. .

Precious Metals Critical raw materialsWhat factors are driving rhodium price trends? [ Read all ]

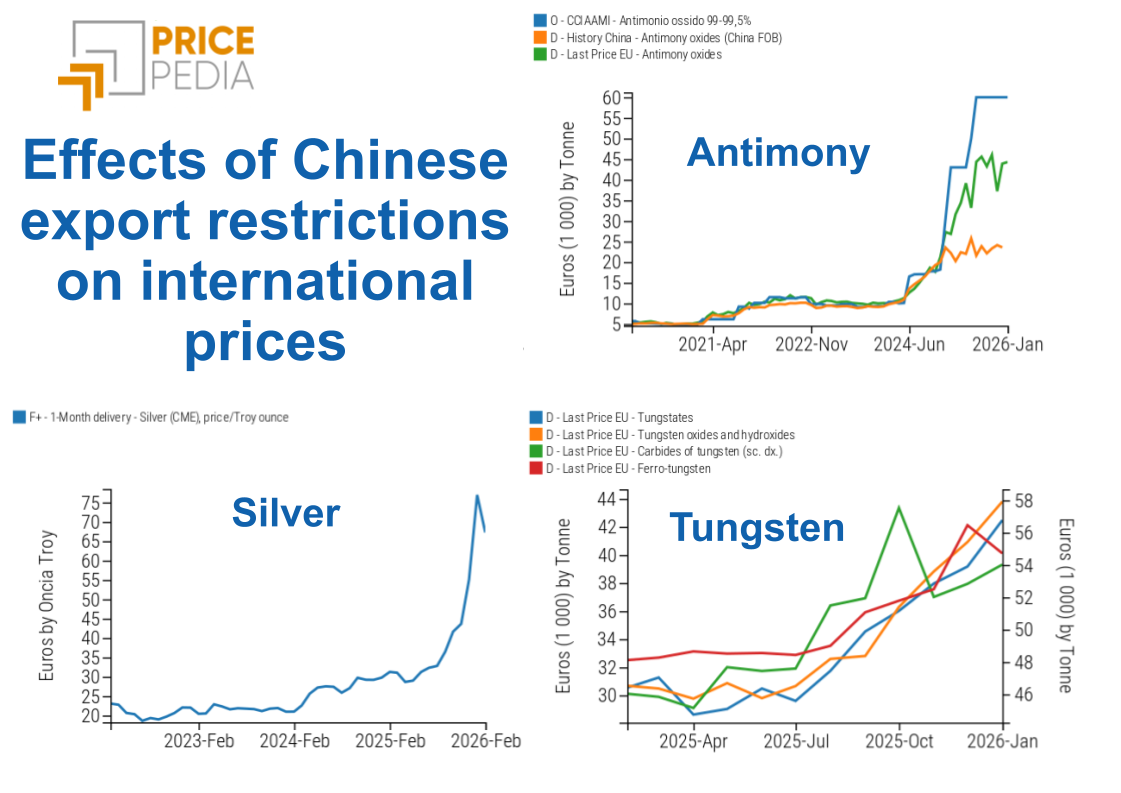

Tungsten, antimony and silver: what do they have in common?

Published by Luigi Bidoia. .

Precious Metals Antimony Tungsten Critical raw materialsLa limitazione delle esportazioni cinesi porta i prezzi mondiali alle stelle [ Read all ]

History repeats itself: uncertainty pushes up gold and silver prices

Published by Luca Sazzini. .

Precious Metals Price DriversHistorically silver has been more subject to speculation than gold [ Read all ]