The Increased Vulnerability of Fuel Prices

The role of the Strait of Hormuz and different market structures in the transmission of energy shocks

Published by Luigi Bidoia. .

Oil Petrolchimica Global Economic TrendsTwo months after the attack by the United States and Israel on Iran and the subsequent blockade of the Strait of Hormuz, it is useful to analyze how increases in oil and liquefied natural gas (LNG) prices — the main energy commodities transiting through the strait — have been transmitted across different energy and petrochemical value chains.

The evidence clearly shows that the transmission of shocks is not uniform: it depends crucially on the structural characteristics of the markets involved, including demand elasticity, the role of inventories, and the degree of integration along the value chain.

1. The initial shock: oil and gas

Over the past two months, from February 27 to the end of April, the price of Brent crude has increased by 63%, while WTI has recorded a similar rise (+60%). Dubai crude has shown a more moderate increase (+54%), but with a different time profile, reflecting its greater exposure to risks related to the Strait of Hormuz.

Over the same period, LNG prices have risen by 58%, while gas traded at the Dutch TTF hub has increased by 43%.

| Oil prices: Brent, WTI and Dubai | Gas prices traded on the TTF and LNG |

|

|

Price dynamics reflect three distinct phases: initially, the emergence of the Iranian threat primarily affected Dubai crude; subsequently, expectations of a truce reduced prices; finally, the failure of negotiations and the naval blockade triggered a new upward phase, more pronounced for oil than for gas, signaling expectations of more persistent supply-side disruptions.

Do you want to stay up-to-date on commodity market trends?

Sign up for PricePedia newsletter: it's free!

2. Transmission to fuels

To assess the transmission of the shock, it is useful to examine petroleum product prices. Data show that in March, gasoline and diesel recorded increases above 50%, while butane (+31%) and propane (+21%) experienced much more limited changes. In April, gasoline continued to rise, while price of liquefied petroleum gases (LPG: butane and propane) remained broadly stable.

Financial pricing of oil derivatives (monthly % changes in dollars)

source: Chicago Mercantile Exchange (CME)

source: Chicago Mercantile Exchange (CME)

This outcome may appear counterintuitive, given that more than 40% of LPG global trade passes through the Strait of Hormuz, compared to around 20% for gasoline and 10% for diesel. The explanation lies in market characteristics.

Transport fuels exhibit rigid demand in the short term, low substitutability, and limited inventory levels. This leads to a rapid and almost complete pass-through of cost increases. By contrast, the LPG market is more flexible: demand is more elastic, alternative energy sources are available, and inventory management is more extensive, all of which help dampen the impact of shocks.

Expectations also play a key role: market participants did not initially anticipate a prolonged closure of the strait, assuming that the global system could rebalance through arbitrage and the reallocation of trade flows.

3. Impact on petrochemical products

The same mechanisms explain the price dynamics of thermoplastics. In March, polypropylene increased by 27%, linear polyethylene by 21%, and PVC by 14%. In April, the first two continued to grow, but at rates below 10%, while PVC recorded a decline of around 4%.

Financial pricing of thermoplastics (monthly % changes in dollars)

fonte: Dalian Commodity Exchange (DCE )

fonte: Dalian Commodity Exchange (DCE )

The lower responsiveness is linked to the greater complexity of the production chain: thermoplastics are derived from processes involving multiple intermediate stages and the use of both oil-based and gas-based feedstocks, resulting in a more gradual pass-through of energy costs.

Moreover, demand is more elastic and closely tied to the economic cycle: sectors such as manufacturing, construction, and durable goods can reduce or postpone purchases. Greater inventory management capacity along the value chain further helps absorb short-term shocks.

Here too, expectations are central: in the absence of prolonged disruption scenarios, markets tend to treat shocks as temporary, limiting the magnitude of price increases.

4. The role of expectations and scenarios

The evolution of the conflict affects prices through two channels: it determines the intensity of the oil shock and shapes its transmission along the value chain.

In a scenario of relatively rapid resolution, the main effect is a structural increase in energy prices driven by a higher risk premium. In this context, pass-through remains high for fuels but more limited for LPG and petrochemical products.

Conversely, in the case of a prolonged or escalating conflict, price effects become broader and more widespread. A prolonged closure of the Strait of Hormuz or a deterioration in Iran’s production capacity would weaken global rebalancing mechanisms, making arbitrage and flow reallocation insufficient.

In such a scenario, LPG and thermoplastics prices would tend to align more closely with oil, with stronger and more persistent increases.

Conclusions

The analysis shows that the transmission of energy shocks depends crucially on market structure. Fuels, LPG, and petrochemical products respond differently depending on demand elasticity, inventory capacity, and the degree of supply chain integration.

These factors determine not only the magnitude of price effects but also their timing and persistence, making it essential to consider the specific characteristics of each market to fully understand the impact of geopolitical shocks.

You may be interested in:

Supply Risk in the Event of a Closure of the Strait of Hormuz

Published by Luigi Bidoia. .

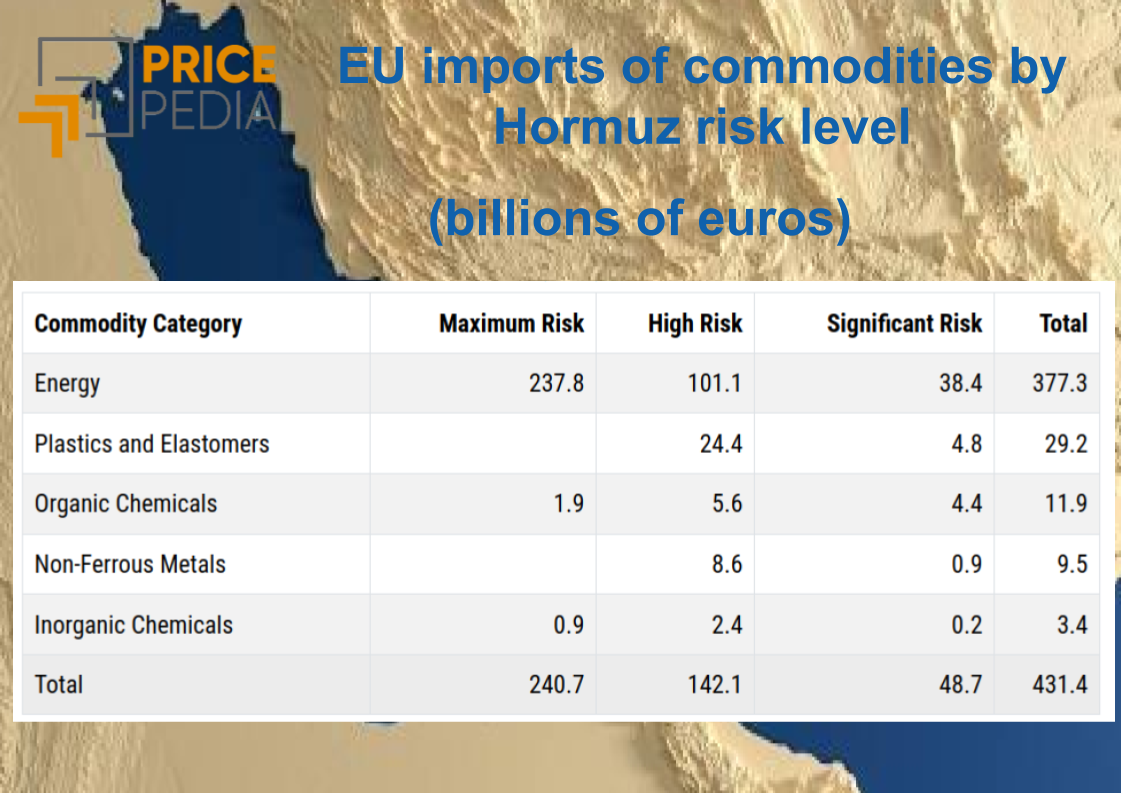

Energy Organic Chemicals Petrolchimica Procurement Risk ManagementLe commodity europee maggiormente esposte al rischio Hormuz [ Read all ]

Maleic Anhydride and UPR Resins: Why China Is Winning the Global Competition

Published by Luigi Bidoia. .

Petrolchimica China in global commodity marketsLo shock energetico attenua solo marginalmente il vantaggio competitivo della Cina nella piattaforma petrolchimica C4 [ Read all ]

Polymer Value Chain: China’s Growing Role

Published by Luigi Bidoia. .

Organic Chemicals Petrolchimica bioplastics basic thermoplastics technopolymers Bio-Based Chemicals China in global commodity marketsIl caso della trasformazione green dell'epicloridrina [ Read all ]