The difficult defense of EU melamine production against China's large-scale economies

Speculation takes advantage of the shift from specific duties to ad valorem tariffs

Published by Luigi Bidoia. .

economic analysis melamine Price DriversBefore the 2022 energy crisis, melamine resins had experienced strong growth in the production of tableware, kitchenware, and furniture laminates. Their lightness, durability, cost-effectiveness, and, above all, ease of decoration and molding made them one of the most innovative raw materials for the home sector. The key component of these resins is melamine, a molecule derived from ammonia which, when combined with formaldehyde and developed through polymerization, forms a cross-linked polymer network that constitutes the basis of melamine resins.

China's success

Melamine resin tableware was a typical product of Western markets in the second half of the 20th century, developed and consumed mainly at a regional level. Its full internationalization took place in the 21st century, driven by the expansion of Chinese production capacity and exports, which transformed this product into a global commodity accessible to emerging markets as well. The strong growth in the production of melamine resin goods created the conditions in China for the large-scale development of the melamine industry. The resulting economies of scale generated a significant competitive advantage, which only countries with competitive access to basic raw materials — particularly ammonia, a key input for melamine production — have been able to match.

EU anti-dumping duties

In response to the growth of Chinese melamine production, major European companies have faced increasing difficulties. The European Commission has attempted to address this trend through the introduction of anti-dumping measures against Chinese producers. The first measure was implemented in 2011 in the form of specific duties (a fixed amount per ton). In 2017, these measures were renewed and extended until 2022. At the time of the 2022 renewal, a new measure was added to the specific duties, consisting of the introduction of a minimum import price. However, the results in terms of protecting the European industry proved to be very limited. This led to a further intervention in 2023, with EU Regulation 2023/2653[1], which updated the list of Chinese exporters subject to measures and introduced more targeted duties. Once again, the results were not satisfactory, prompting a new intervention with EU Regulation 2025/325[2]of February 18, characterized by the introduction of ad valorem duties of up to 65%.

The effects of these protectionist policies can be analyzed through two main sets of data:

- a comparison of sales in the EU market and in extra-EU markets of the main competing countries

- import prices and domestic EU prices

Sales in the EU and extra-EU markets of the main competing countries

The two charts below show, respectively, the evolution of melamine exports to the EU internal market and to extra-EU markets.

The charts clearly highlight the success of the Chinese industry, initially in extra-EU markets and, after 2020, also in the EU internal market. As early as the beginning of this century, China was already competing on equal terms with leading European producers — particularly German and Dutch companies — in extra-EU markets. As the Chinese melamine industry continued to develop, exports entered a phase of strong growth that has persisted to the present day. In contrast, extra-EU exports by European producers remained relatively stable, before turning into a clear decline in recent years.

Do you want to stay up-to-date on commodity market trends?

Sign up for PricePedia newsletter: it's free!

The success of Chinese companies in the EU market, up to the energy crisis that began in 2021, was contained by anti-dumping policies. Subsequently, as international melamine prices increased sharply, the price limits imposed on Chinese exporters were largely exceeded by EU domestic prices, leading to a surge in EU imports from China. The new 2025 regulation replaced price limits and specific duties with ad valorem duties, expressed as a percentage of import value. This led to an initial containment of imports from China, but also to a simultaneous and significant increase in prices in the EU market.

International and EU domestic melamine prices

The two charts below show, in the first case, a comparison between Chinese export FOB prices (international benchmark), EU import CIF prices from extra-EU countries, and intra-EU transaction prices (Last Price EU, calculated as the average between CIF and FOB prices). The second chart presents the same EU import and intra-EU prices, comparing them with distribution prices recorded by the Milan Chamber of Commerce.

International and EU prices for melamine

| International prices | EU prices |

|

|

The analysis of these data highlights the following key points:

- China has consistently exported at prices significantly lower than those of other international competitors (represented by CIF prices of EU imports from extra-EU countries) and, above all, lower than intra-EU transaction prices;

- Chinese prices have systematically anticipated changes in both international prices and EU domestic prices, confirming China’s role as the leading country in the global melamine market;

- the introduction in February 2025 of anti-dumping ad valorem duties on Chinese imports led to a significant increase in intra-EU transaction prices, which are representative of producer prices in the EU market. However, this increase moderated between the end of 2025 and the beginning of 2026;

- the introduction of duties had an even stronger impact on EU distribution prices, whose increases were significantly higher than those observed at the production level, suggesting the presence of possible speculative behaviors. Moreover, while producer prices declined significantly between the end of 2025 and early 2026, distribution prices — even in the March 2026 survey — remained broadly unchanged compared to the levels recorded in spring 2025.

Conclusions

Over the course of this century, one of China’s most successful products in global markets has been melamine-based manufactured goods. This has allowed the country to fully exploit economies of scale in melamine production — the key raw material of these resins — providing Chinese companies with a significant cost advantage.

The EU’s attempts to protect the European melamine industry proved moderately effective within the EU market until 2020, but contributed to a weakening of EU companies’ competitiveness in extra-EU markets. After 2020, the barriers protecting the EU market — based on minimum prices and specific duties — became ineffective in the face of rapidly rising international and domestic prices, which more than doubled in less than two years.

The response of the European Commission, also under pressure from European producers, was to replace price-based barriers with ad valorem duties, expressed as a percentage of import value. This measure led to an initial reduction in import flows from China, but also created the conditions for potential speculative behavior, particularly at the distribution level.

[1] Commission Implementing Regulation (EU) 2023/2653 of 27 November 2023 amending Implementing Regulation (EU) 2023/1776 imposing a definitive anti-dumping duty on imports of melamine originating in the People’s Republic of China following a new exporter review pursuant to Article 11(4) of Regulation (EU) 2016/1036 of the European Parliament and of the Council

[2] Commission Implementing Regulation (EU) 2025/325 of 18 February 2025 amending Implementing Regulation (EU) 2023/1776 imposing a definitive anti-dumping duty on imports of melamine originating in the People’s Republic of China, following a partial interim review pursuant to Article 11(3) of Regulation (EU) 2016/1036 of the European Parliament and of the Council

You may be interested in:

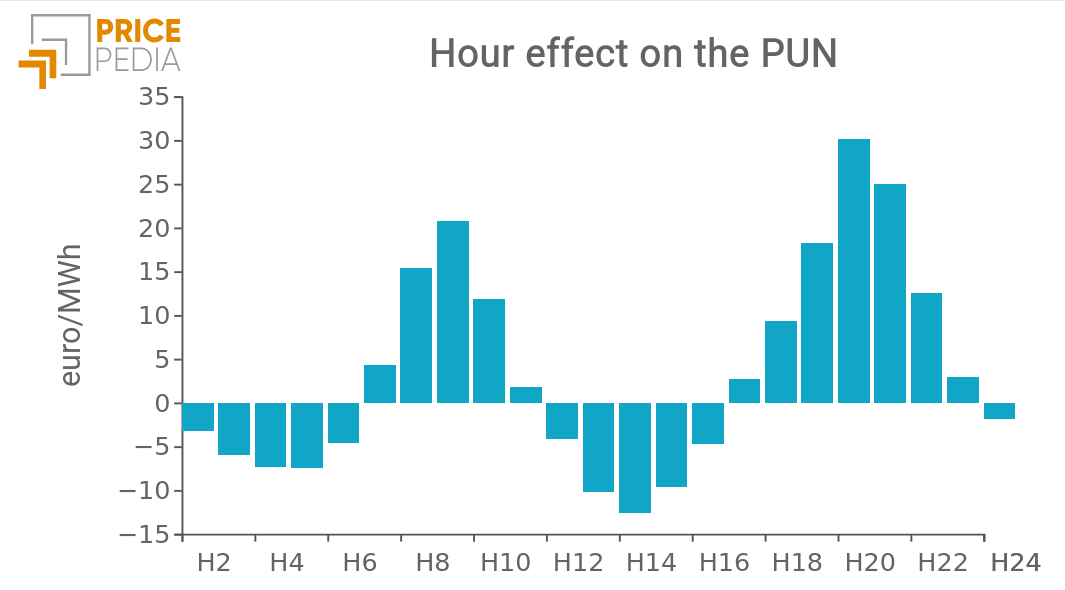

Hourly PUN price: is there a specific “hour” effect?

Published by Emanuele Morelli. .

Electricity's National Single Price Electric Power economic analysis Machine learning and EconometricsAn econometric analysis reveals the existence of a temporal pattern in electricity prices. [ Read all ]

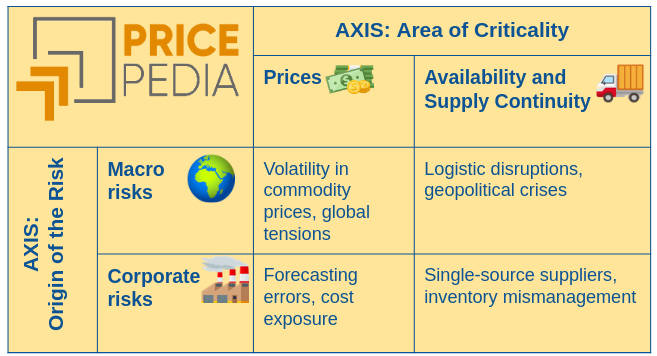

Macro commodity risks and corporate procurement risks

Published by Cristina Luca. .

Procurement economic analysis Procurement Risk ManagementHow procurement management is evolving in an uncertain world [ Read all ]

Physical Prices, Financial Prices, and Risk Transmission: An Analysis of Correlations

Published by Cristina Luca. .

economic analysis Analysis tools and methodologiesAnalisi quantitativa delle correlazioni tra prezzi fisici e finanziari [ Read all ]