The Price of Sulfur: How to Measure It in a Market Without a Public Benchmark

Geopolitical tensions bring sulfur back into focus as a critical commodity

Published by Luigi Bidoia. .

Sulphuric acid industry Analysis tools and methodologies

Among the prices reacting to the ongoing conflict involving the United States, Israel, and Iran, sulfur is one of the most sensitive and strategically relevant. The recent attention on this commodity has highlighted a specific issue related to the measurement of economic phenomena. Despite being widely traded at the international level, sulfur does not have a public and transparent price benchmark. Unlike many other raw materials, there is no liquid futures market for sulfur, and the main price references are provided by specialized agencies through paid information services.

This situation creates an information challenge for companies that use or purchase sulfur and that, especially in a delicate phase like the current one, need reliable indicators. The key question therefore becomes: how can price developments be monitored in a market where the most relevant information is private?

The case study described in this article shows how, even in contexts like this, useful information can be reconstructed by combining different sources and using simple statistical tools. The objective is not to replace professional paid sources, but to build an analytical framework capable of providing coherent, timely, and operationally useful signals.

Two Complementary Information Sources

In the case of sulfur, two types of data are particularly useful for monitoring price developments.

The first consists of CFD-type prices (Contracts for Difference), published by information platforms and economic websites such as Trading Economics and other international data providers. A CFD is a financial derivative whose price generally reflects that of a cash-settled futures contract. In both cases, those who buy or sell these instruments realize gains or losses solely from price changes, without any physical exchange of the commodity.

However, there are important differences in market structure and guarantee mechanisms. While futures contracts are traded on regulated exchanges (such as the Chicago Mercantile Exchange – CME or the Intercontinental Exchange – ICE), CFDs are traded OTC (over-the-counter), directly between market participants, typically through brokers.

These prices usually reflect the conditions prevailing in the trading and wholesale distribution markets. Their main advantage is timeliness, as they are updated frequently. However, they also present an important limitation: the methodology used to construct these prices is not always fully transparent.

The second source consists of customs prices, which record the average values of import and export transactions. In the case of sulfur, two indicators are particularly useful:

- Chinese import prices (CIF);

- intra-EU trade prices.

These data reflect actual transactions between economic operators and therefore represent a transparent and verifiable source of information. However, they also have a limitation: they become available with a certain delay compared to the moment when the commercial negotiation takes place.

Do you want to stay up-to-date on commodity market trends?

Sign up for PricePedia newsletter: it's free!

Comparing the Price Series

In the chart below, the two customs price series (China CIF and intra-EU) are compared with the sulfur CFD published by Trading Economics.

This graphical comparison provides an initial and relevant insight into the structure of the market.

Sulfur: Comparison of CFD Prices and Customs Prices

The different sources show a very similar pattern over time, indicating that they all reflect the same global sulfur market. However, some interesting differences also emerge.

First, CFD prices are generally higher than customs prices. This is consistent with the fact that they reflect the level of the trading and distribution market, where the price of the raw material typically includes additional commercial and logistical margins.

Second, these prices appear more volatile, reacting more rapidly to changes in market conditions.

A particularly interesting episode emerges at the end of 2017. During that period, the CFD price shows an attempt to increase that is not confirmed by the prices of physical transactions recorded in customs data. This suggests a commercial attempt to raise prices that was not supported by actual market demand.

The comparison between different sources therefore allows not only the monitoring of price levels, but also a better interpretation of market dynamics.

Statistical Evidence: A Globally Integrated Market

A further step in the analysis consists in measuring the correlation between the different price series. The figure below reports the correlations between the three prices considered. The CFD price is also examined by introducing a lag of one, two, and three months.

The results show very high correlations. In particular, the correlation between Chinese import prices and intra-EU trade prices reaches values close to 0.97, indicating an almost perfect synchronization.

Correlation between sulfur CFD prices and customs prices

This result suggests that the sulfur market, despite the absence of an official public benchmark, is strongly integrated at the global level. Prices across different geographical areas tend to move almost simultaneously, indicating that international trade and trading activity allow a rapid transmission of price information.

The Logistical Lag in Customs Prices

The analysis becomes even more interesting when introducing a simple time comparison. When the CFD price is lagged by one month, its correlation with customs prices increases further. This result is consistent with the physical structure of the international sulfur trade.

The price recorded by traders reflects the moment when the cargo is negotiated in the market. Customs prices, by contrast, reflect the value of the cargo at the time of import, which occurs several weeks later.

Considering that the main sulfur trade routes (for example from the Middle East to Asia and Europe) typically require several weeks of maritime transport, the lag observed in monthly data appears perfectly plausible.

A Model of the Sulfur Market

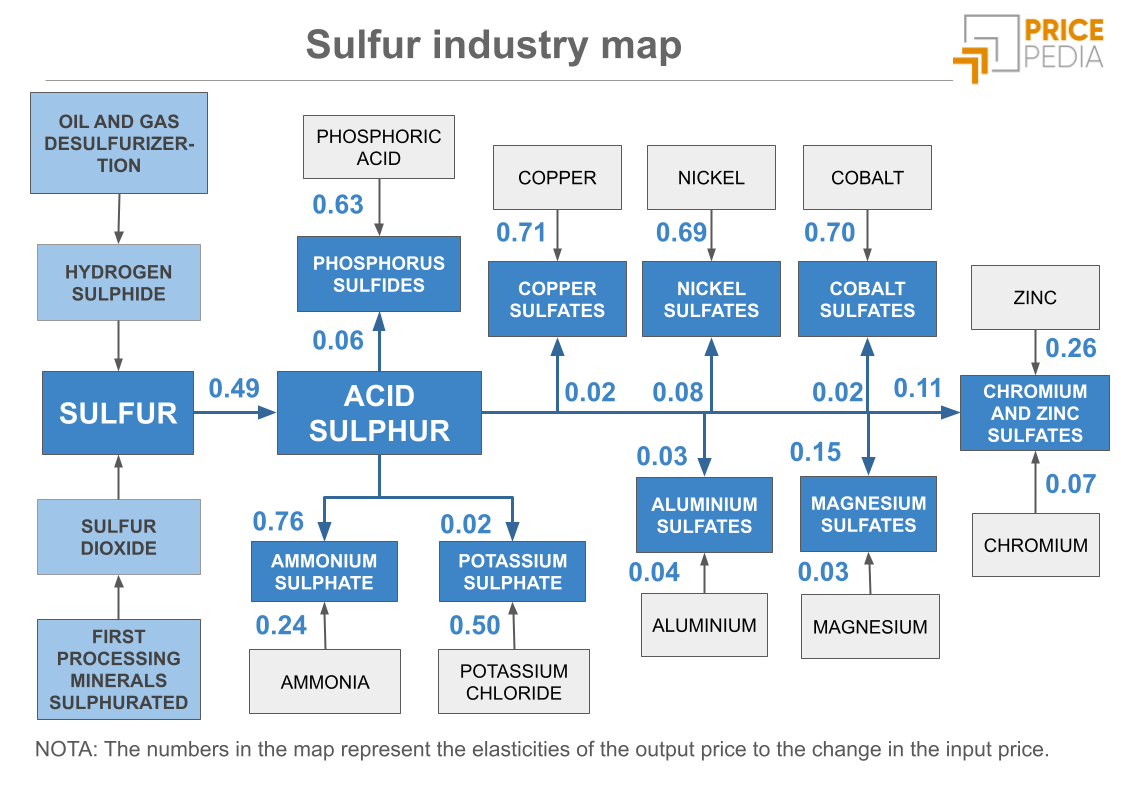

By combining all this evidence, it is possible to outline a simple model of how the global sulfur market operates. Prices are initially formed in the market for cargoes exported from the main producing regions, particularly the Middle East. International traders negotiate these cargoes and quickly transmit the resulting price signal to wholesale markets.

After maritime transport, these prices are then reflected in the customs statistics of importing countries.

Useful Information for Companies

The analysis suggests several operational insights for companies that use sulfur directly or rely on its derivatives. CFD prices published by traders and data providers can be used as leading indicators of market developments. Customs data, on the other hand, provide a useful tool for validating and confirming the observed price trends.

The combination of these two sources therefore makes it possible to obtain a more comprehensive view of the market, even in the absence of official public benchmarks.

This case illustrates how the integration of public data and relatively simple analytical tools can provide valuable information for corporate decision-making processes, even in commodity markets characterized by a high degree of information opacity.

You may be interested in:

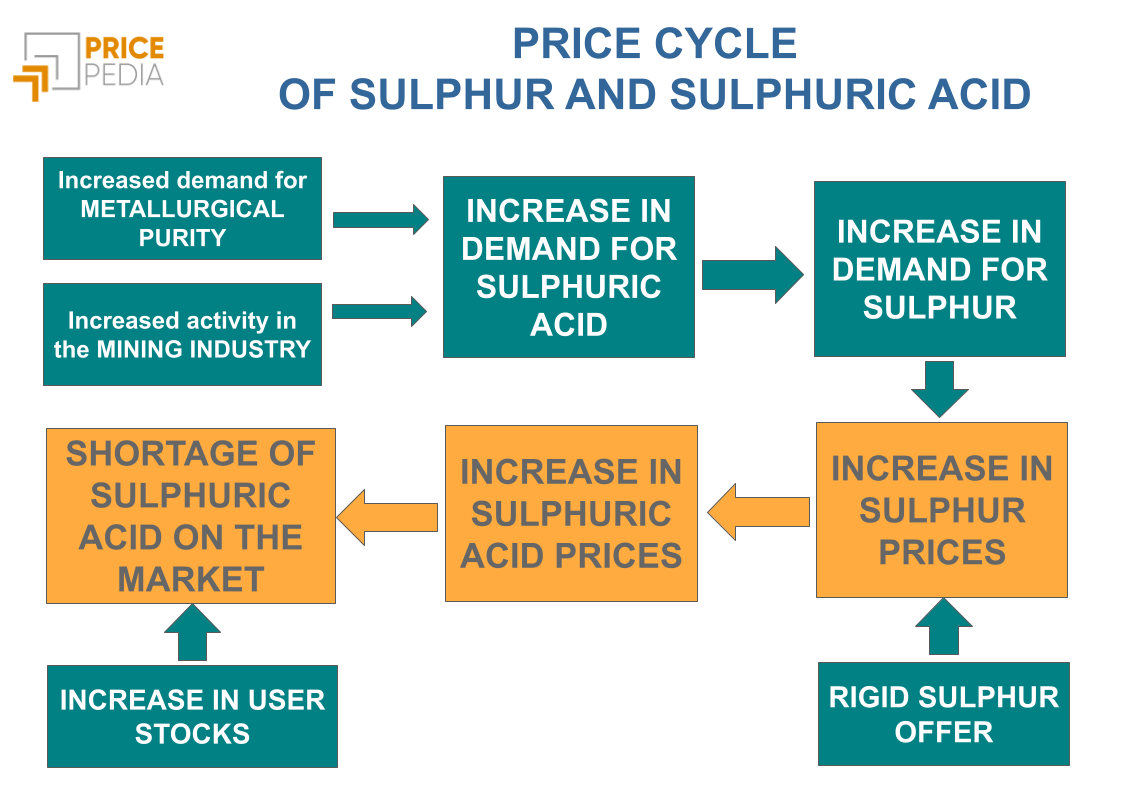

Sulphuric acid: product scarcity and cost increases drive current high prices

Published by Luigi Bidoia. .

Sulphuric acid industry Price DriversAumenti dei prezzi molto differenziati per area geografica e fase della distribuzione [ Read all ]

Sulfur prices: a new global uptrend cycle?

Published by Luigi Bidoia. .

Fertilizers Sulphuric acid industry Price DriversAfter the peaks of 2008 and 2022, international quotations exceed €250/ton, signaling the start of an intense phase driven by rigid supply and volatile demand [ Read all ]

Tensions in the Global Sulfur Market and Impacts on the Chemical Supply Chain

Published by Luigi Bidoia. .

Sulphuric acid industry Cost pass-throughIl basso prezzo dell'acido solforico attenua gli effetti del ciclo dello zolfo sui derivati [ Read all ]